In recent weeks, the municipal bond market has faced an unprecedented tumult, one that is sparking conversations not just among investors, but also among policymakers and financial analysts. What makes this moment especially fascinating—and alarming—is that yields have experienced fluctuations rarely seen before, compressing and expanding in response to ever-changing government actions. The core of this uncertainty lies in the volatile nature of economic policies and their implications on the municipal securities market, and what we are witnessing is more than just financial adjustments; it’s a manifestation of the fundamental unpredictability that pervades our economic climate.

Firstly, triple-A yields plummeted significantly—anywhere from 30 to 50 basis points—within a matter of hours, erasing Wednesday’s losses and sending shockwaves across the market. This raises a crucial question: are municipal bonds still a reliable investment in these chaotic times? As someone who leans toward center-right economic principles, I find myself increasingly skeptical about government interventions and their long-term sustainability. Instead of creating a stable environment, such dramatic policy shifts, like President Trump’s 90-day tariff respite, often lead to knee-jerk reactions that further destabilize the markets.

The Anemic Performance of Munis

Recent data has revealed alarmingly poor performance metrics for municipal bonds. For example, during the first three days of the week, yields surged by around 90 basis points—marking one of the largest shifts recorded in over 45 years. This drastic adjustment reflects not just the panic of today’s investors, but also the accumulated stress from previous months of uncertainty. What was particularly telling was Monday’s performance, which recorded a disheartening negative return of 2.85%—the worst one-day performance in over three decades. When investors are unable to move their assets effectively, it raises questions about the liquidity of the market itself.

Shouldn’t we be wary when the sector that is supposedly a safe-haven for investors begins to exhibit characteristics of a speculative gamble? This turmoil emphasizes the necessity of robust financial frameworks that disincentivize such volatility, rather than rewarding the player who can react the fastest to policy changes.

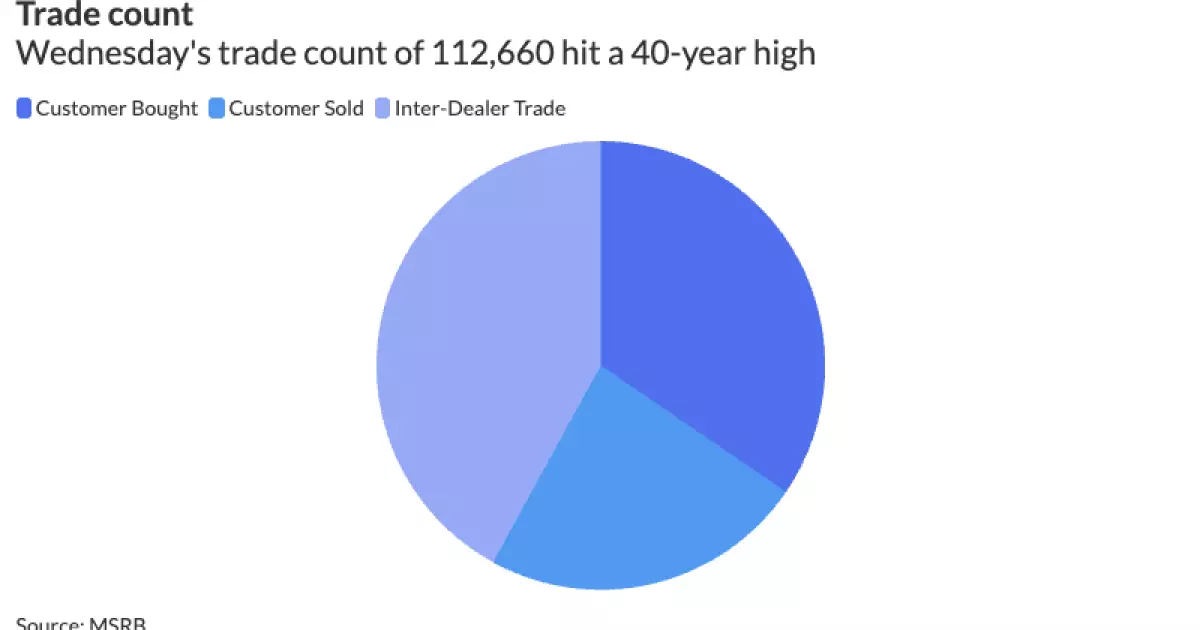

The Record-Breaking Trading Activity

Interestingly, Wednesday marked a notable uptick in trading activity, setting a record of 112,600 trades—the highest since 1995—and this audacity came with $32.5 billion changing hands. On the surface, such figures may signify a vibrant market; however, they also expose underlying issues of desperation and rash decision-making among investors. With the municipal bond market being relatively thinly traded compared to other asset classes, these kinds of spikes raise eyebrows regarding the quality of trades taking place.

The real paradox here lies in the elevation of bid-wanted activity. Even with the so-called safety nets put in place by the White House, bid-wanted levels remained high at $2.9 billion, indicating investor fears and the pressure to liquidate positions. This status quo cannot continue if the market wishes to maintain its veneer of stability. Instead of being a refuge for risk-averse investors, the municipal bond sector risks being tainted by the volatility typical of far more aggressive trading environments.

Questioning the Government’s Role

Also notable is how the market reacted to governmental interventions, such as the aforementioned tariff extension. While it ostensibly calmed fears and provided a pause, it merely postponed dealing with the underlying issues causing market fluctuations. Repeatedly putting a bandage over a deep cut does not heal it; rather, it fosters long-term resentment toward a system that seems to favor knee-jerk responses over sustainable solutions. Center-right principles champion the idea of limited government—shouldn’t we therefore demand clarity and foresight from our elected officials?

As the market muddles through its current cycle of uncertainty, we must critically engage with the narrative being spun around these municipal markets. Investors deserve clarity, not a ping-pong match dictated by political maneuvering. In such an investment landscape, where even established players like BlackRock are wary of market liquidity, the stakes are too high not to scrutinize the long-term implications of these hurried decisions.

Striving for Market Integrity

Ultimately, as a conscious participant in this financial ecosystem, we owe it to ourselves to advocate for genuine systemic reform. If the municipal bond market wishes to regain its reputation as a safe and dependable arena for investment, it must shed the trappings of abrupt volatility and confront the challenges of operational integrity with rigor and foresight. With even the smallest tweak echoing throughout the market, stakeholders need not only be agile; they must also be wise. The current trajectory of municipal bonds is anything but stable, and unless there is a recalibration of how we approach risk and governance, we may just find ourselves in an environment where uncertainty reigns supreme.