The municipal bond market in 2025 is nothing short of a pressure cooker, burdened by an unprecedented surge in issuance that threatens to unsettle an already fragile fixed income landscape. Projections for total municipal issuance have been repeatedly revised upward this year, reaching a staggering forecast of $580 billion from an earlier $520 billion estimate. This dramatic increase is neither accidental nor sustainable. It reflects the fiscal strains local governments face amid rising infrastructure demands and pension obligations. Yet, instead of a smooth absorption by investors, this glut of supply has led to significant underperformance of tax-exempt munis compared to their Treasury counterparts.

The typical dynamic of demand and supply is fundamentally out of whack. While new issuance soared in the first half of the year, reaching nearly $275 billion, redemptions and coupon payments have struggled to keep pace, especially in the crucial months ahead. The expectation of $308 billion in new issuance against $337 billion in redemptions in the latter half of the year suggests potential relief, but this is offset by the fact that Barclays anticipates a 10% drop in issuance in the coming months. The sheer volume of bonds flooding the market is eroding investor confidence, a situation intensified by tax-exempt bonds’ increasingly unattractive valuation relative to U.S. Treasuries.

Tax-Exempt Munis: An Overlooked Underperformer

Municipal bonds—historically a stalwart of conservative portfolios—have become a quiet embarrassment for fixed income investors. Year-to-date returns have been negative, exposing a vulnerability often overshadowed by the high-profile movements of equities or Treasuries. Despite being the only fixed income asset class to post negative total returns this year, the muni market continues to trap overly optimistic investors hoping for a swift rebound.

The fundamental issue is that the market is not just reacting to macroeconomic shifts but structural imbalances. Heavy issuance dilutes value, driving up muni-to-Treasury ratios significantly—10-year ratios creeping toward 77%, and 30-year bonds nearly matching Treasuries at 94%. These elevated ratios are alarming indicators of muni yields underperforming relative to the broader risk-free benchmark. For the cautious, tax-exempt munis increasingly look more like risky credit bets than safe harbingers of stable income, undermining their historical appeal.

Market Nuances and Seasonal Fluctuations

Seasonal patterns in municipal bond markets traditionally offer some reprieve, with July often witnessing declines in muni-to-Treasury ratios and a modest recovery in performance. Historical data excluding the pandemic year illustrates a trend where ratios tend to dip 2 percentage points in July and experience some selloff in August. This pattern coincides with a temporary “breather” where supply slackens, and heightened redemption activity aids market balance.

But this seasonal optimism must be taken cautiously. While strategists at Barclays and BofA acknowledge stronger market technicals during mid-year due to redemptions offsetting supply, the long-term outlook is less sanguine. Expected weakness in market fundamentals as supply outstrips redemption starting September is a major flag for a potentially turbulent autumn. Investors fixing their sights on this seasonality may find themselves blindsided if these anticipated supply-demand dynamics do not materialize as expected.

Interest Rates and Valuations: The Silent Threat

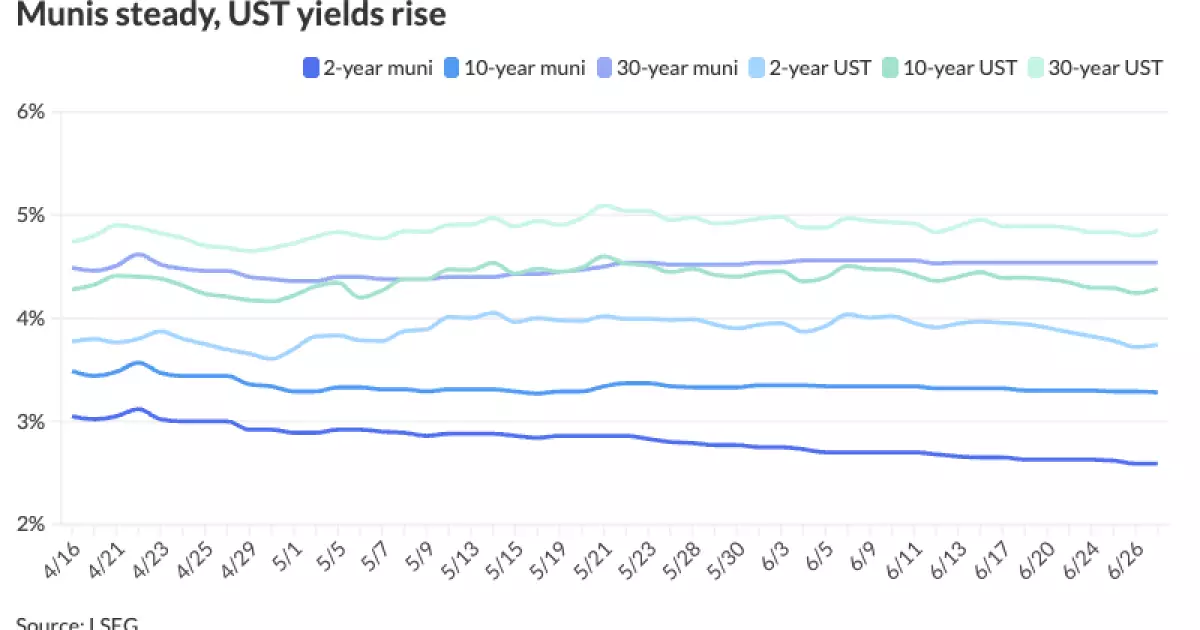

The overlooked elephant in the municipal market room is interest rate risk. Despite a market narrative suggesting that rates are relatively stable—fueled by record high Treasury benchmarks in equities pushing indices like the S&P 500 and Nasdaq to record levels—municipal investors face a stealthy adversary. Treasury yields across maturities have edged notably higher; two-year notes smoothed over 3.74%, and 30-year yields inched close to 4.85% just before market close, signaling tightening financial conditions.

Tax-exempt yields, while only marginally adjusted in basis points, must be scrutinized in context. The AAA municipal scales have nudged up in the range of one to two basis points, which might appear negligible but contribute significantly over time to the poor total returns muni investors currently face. The risk-adjusted return calculus is now less favorable, especially for long-duration municipal holders, who may find themselves increasingly exposed if interest rates remain elevated or rise further.

Structural Risks Beyond Supply and Rates

This crisis is about more than issuance volume and interest rates; it is symptomatic of deeper structural fissures in public finance. Municipal bonds remain tethered to the financial health of local governments, many of which grapple with mounting pension liabilities, uncertain federal support, and pressure to fund social services amid shifting political priorities.

The willingness of investors to absorb growing issues at current yields undermines the market’s very function as a barometer of public creditworthiness. Instead, it risks creating a bubble where risk is invisibly underpriced. Overreliance on a “back-loaded” recovery assumes a cooperative confluence of technical factors—an assumption unworthy of blind trust in a capital market as complex and politically influenced as municipal bonds.

Why a Center-Right Perspective Demands Skepticism

From a pragmatic center-right viewpoint that values fiscal responsibility and market discipline, the municipal bond market’s current trajectory is troubling. The toleration of such high issuance levels without meaningful market repricing sends the wrong signal to policymakers: that debt can be expanded indefinitely without consequence. This complacency could delay necessary reforms in public sector spending and borrowing practices, placing future taxpayers at risk.

Moreover, pushing investors toward longer durations in a market fraught with uncertainty and historically low returns seems misguided. It encourages a form of yield chasing detached from true risk assessment. For investors who value prudence and capital preservation—core conservative financial tenets—the municipal bond market right now offers a cautionary tale about chasing perceived bargains without acknowledging the broader systemic risks.

The call to “get longer” into 2H25, while potentially valid from a strictly technical perspective, overlooks the essential narrative that public finance is entering a new era of stress and volatility not effectively priced into current muni valuations. Investors and policymakers alike should heed this warning, lest the “safe” municipal bond market become an unforeseen source of financial instability.