The municipal bond market, often hailed as a reliable harbor for conservative investors, is currently navigating a surprisingly turbulent undercurrent. While surface-level observations suggest a relatively steady environment with limited volatility, a closer examination reveals that the muni market is quietly grappling with structural and technical challenges that could dampen its traditionally stable allure. Behind modest yield movements and consistent fund inflows, cracks are forming that demand a more skeptical and discerning investor outlook.

Yield Ratios and After-Tax Spreads: An Illusion of Cheapness

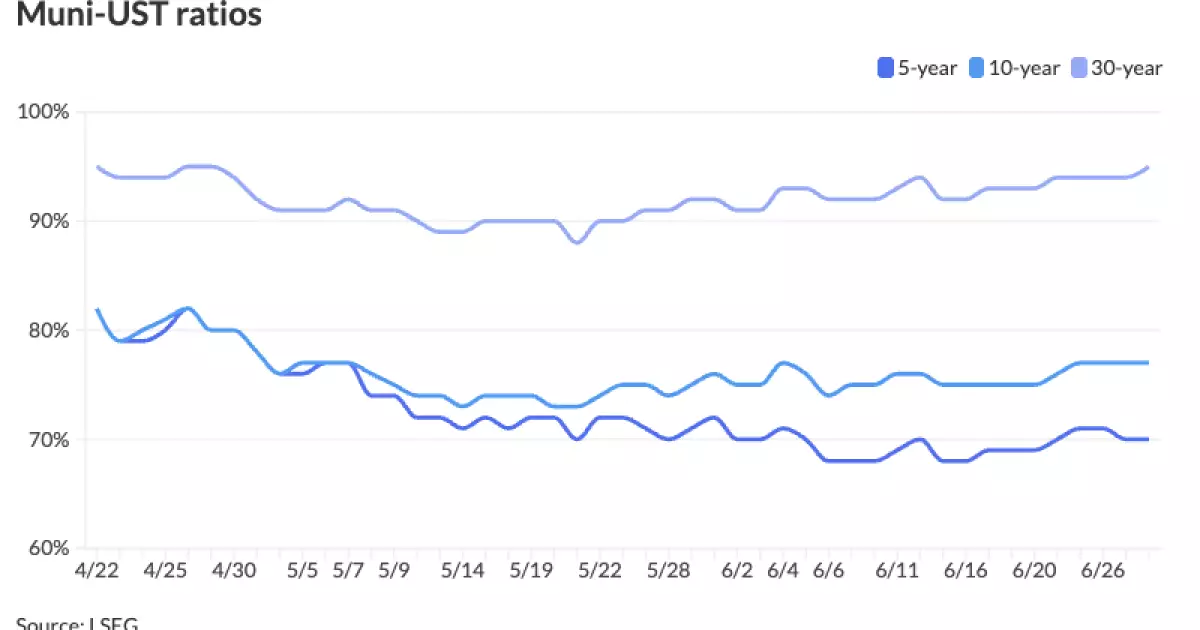

One of the more concerning phenomena is the widening of two-, five-, and ten-year muni-to-Treasury yield ratios, hovering between 66% and 77%, while the 30-year ratio approaches 95%. At first glance, these figures suggest that municipal bonds are cheap relative to Treasuries, theoretically offering an opportunity for yield-hungry investors. Yet, this cheapness is more a symptom of uncertainty than bargain hunting. The stubbornly wide spreads, especially on the long end, underscore investor hesitance to embrace munis aggressively, likely due to macroeconomic headwinds and a lack of a clear catalyst to send yields lower.

After-tax yields on many high-grade municipal deals surpass 8% on a tax-equivalent basis—an impressive figure in today’s low real return environment. However, without stronger technical support, these seemingly attractive levels risk turning into yield traps. The cautious tone among dealers and portfolio managers suggests that despite strong inquiry for “anything attractively priced,” real conviction is missing, revealing a market stuck in limbo.

Inflows: Cautious Optimism Amid Modest Fund Flows

Investor participation remains tepid rather than robust. Municipal mutual funds have posted their ninth consecutive week of net inflows, totaling around $77 million last week, maintaining a positive but uninspiring trend. To put that in perspective, the level of inflows pales compared to the scale needed to ignite sustained muni outperformance or significant rally. It’s a whisper where a roar is needed. The cumulative result—a modest 0.19% gain last week and a slight negative year-to-date return of 0.45%—speaks volumes about investor sentiment: cautious but non-committal.

This subdued demand, despite a technically strong environment in terms of upcoming July reinvestments amounting to roughly $40 billion in principal and $14 billion in interest, tells a story of fragmented investor confidence. Large redemption volumes from key states like California, New York, and Florida indicate significant liquidity shifts, yet the demand side hasn’t adapted aggressively to mop up supply or push prices meaningfully higher.

Primary Market Activity: Deals Without Firepower

New issuance remains another point of contention for the muni market’s vigor. With just $2.5 billion in primary issuance expected during a holiday-shortened week, liquidity dynamics skew toward a buyer’s market. While this might offer respite to existing holders, it also dampens excitement as the pipeline lacks blockbuster deals that can attract fresh capital or spark sustained momentum.

Looking ahead, large deals from California, Washington, New York, and Honolulu promise to inject some life back into the supply-demand equation. Yet even these significant transactions—while eagerly anticipated—are no guarantee of rekindling strong momentum or attracting a broader investment base. The market’s current technical strength is thus largely a function of limited alternatives rather than genuine enthusiasm.

Strong Technicals: A Double-Edged Sword

Notably, the July reinvestment window, buoyed by the redemption of $33 billion in maturing and called bonds, positions the municipal space to absorb new issuance with relative ease. This influx of cash should provide immediate support, fostering a technical backdrop that could be described as “decidedly positive” by market strategists.

But here lies the rub: such technical strength, while comforting, masks an underlying fragility. The market’s ability to rally in the near term is conditional on the absence of macroeconomic shocks and continued steady fund flows. The current state resembles a market held together by momentum and investor necessity rather than conviction or fundamental strength. In the center-right perspective that values sustainable growth and cautious optimism, this reliance on technical support over fundamentals should be viewed with skepticism.

Comparisons with Treasuries: Dangerous Complacency

U.S. Treasuries have experienced a gentle rally, with yields falling across the curve by several basis points. This decline contrasts with municipal yields inching higher by up to two basis points, fostering a slight pickup in relative attractiveness. Yet, relying on this comparative cheapness ignores that Treasuries remain more liquid and less vulnerable to idiosyncratic credit risks haunting munis.

Investors should resist the temptation to chase muni yields purely based on ratio comparisons. The potential for spreads to widen further—and for muni yields to rise in response—remains tangible, particularly if inflation or interest rate dynamics shift unfavorably. A center-right investor mindset calls for prudence, emphasizing risk-adjusted returns and a healthy discount for municipal securities’ structural complexities and fiscal exposures.

The Road Ahead: Selective Caution Over Blind Optimism

From this vantage point, the municipal bond market appears caught between opportunity and risk. The technical forces of reinvestment dollars and subdued issuance provide momentary lulled comfort. Simultaneously, fundamental issues such as widening yield spreads, subdued inflows, and fragile investor conviction warn against complacency.

For investors navigating this terrain, the lesson is clear: municipal bonds must be approached with selective caution. Not all muni sectors or credits will weather latent stresses equally, and high yields should not tempt a wholesale rush. Rather, discerning allocation with a focus on resilient credits and awareness of macroeconomic sensitivities aligns best with conservative yet informed investment philosophies. The municipal market’s current veneer of stability should not obscure its underlying vulnerability.