The municipal bonds market recently witnessed some noteworthy developments influenced by myriad factors, including fluctuations in U.S. Treasury yields and variations in primary market supply. This article aims to provide a comprehensive analysis of the current dynamics within the municipal bond sector, exploring the impacts of new issuances, investor appetite, and market ratios.

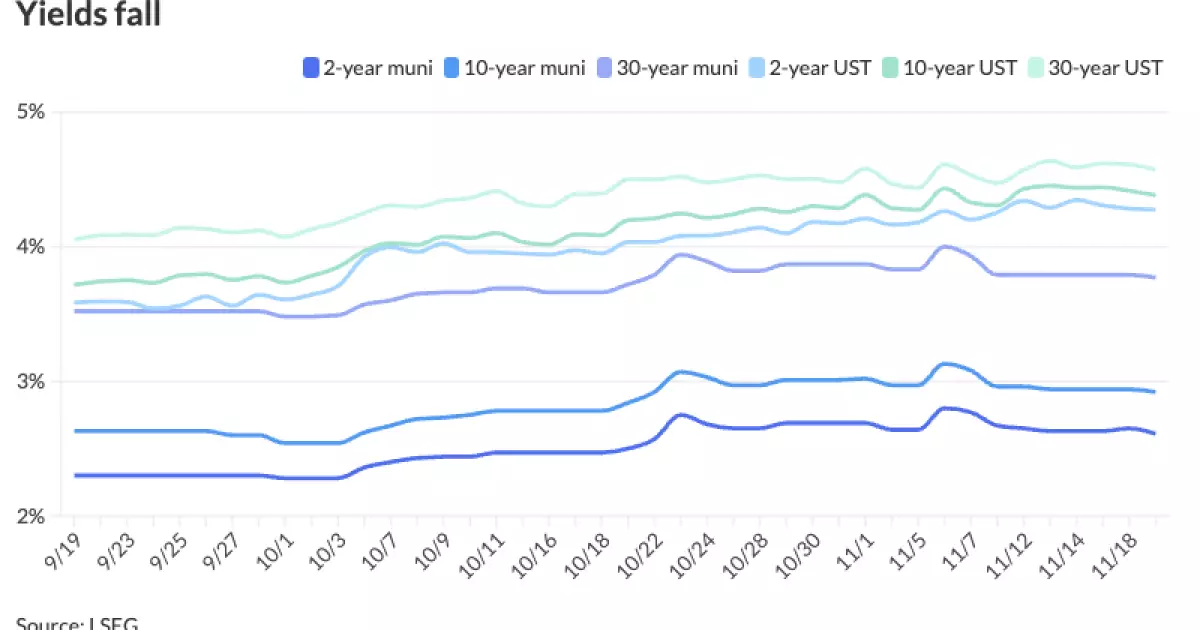

This past Tuesday, municipal bonds showed improvement in parallel with a drop in U.S. Treasury (UST) yields, leading to a generally favorable environment for municipal issuers. As Treasury yields fell, Triple-A municipal yields experienced an uptick ranging from one to six basis points across various points on the yield curve. This interplay indicates a nuanced relationship where declining UST yields often enhance the attractiveness of municipal bonds, as they offer relatively higher yields in a low-rate environment.

Interestingly, the secondary market’s activity was subdued as attention shifted to the primary market where significant new issuances captured investor interest. Notably, the $1 billion United Airlines Terminal project in Houston successfully attracted robust demand, showcasing the ongoing investor appetite for well-structured municipal projects, despite a lighter issuance calendar compared to previous weeks.

According to Chris Brigati, a senior figure at SWBC, a “reasonably decent week of supply” underscores the underlying investor demand for new issues. His assessment highlights a pent-up demand for municipal bonds, suggesting that upcoming issuances are likely to be absorbed effectively, thereby keeping market ratios tight and limiting the availability of bonds for purchase. This sentiment is echoed by Matt Fabian of Municipal Market Analytics, Inc., who commented on the prevailing rich ratios in shorter maturities, indicating that the market is tending toward an environment where demand consistently outstrips supply.

Current municipal bond ratios reflect varying dynamics: the two-year municipal to UST ratio stood at 61%, climbing to 82% for the 30-year maturity. Such inflated ratios not only demonstrate the competitive nature of munis but also signify that while yields may appear attractive, they have entered what can be termed a “uniformly rich” territory. This could suggest caution for prospective buyers looking to capture value at this juncture.

Last week revealed contrasting trends in fund flows, as retail demand appears robust, particularly in separately managed accounts. Interestingly, mutual funds and exchange-traded funds (ETFs) saw modest inflows, reinforcing the notion of sustained interest in municipal bonds despite broader economic uncertainties. Conversely, money market funds experienced outflows, possibly reflecting investor behavior that seems to prioritize seeking better income opportunities.

The sustainability of mutual fund inflows remains uncertain as the year draws to a close. Notably, they are on track for approximately $30 billion in inflows—a figure that is relatively impressive when compared to historical data over the past 15 years, where only four years have seen better performance.

Looking ahead, the upcoming weeks are pivotal as the market anticipates increased supply. Any substantial rise in issuance could have repercussions on yield levels and overall bond performance. Notably, from November last year through year’s end, approximately $45 billion of supply entered the market, raising questions about how this year’s issuance will evolve in light of potential tax-exemption changes that could further entice issuers to enter the market.

Projected supply for this year could potentially reach the substantial figure of $500 billion. To achieve this, however, yields must remain in check. As Fred Fabian pointed out, incremental price declines or yield hikes may be necessary, especially amidst ongoing concerns related to inflation and credit risks affecting USTs.

In the primary market, several large-scale municipal projects launched recently, including a $1.1 billion revenue bond for United Airlines and a $782 million green energy project in California. Such projects signify the diverse array of funding needs present in today’s economy, spawning significant investor interest.

Moving to competitive sales, the Delaware Transportation Authority successfully auctioned $153.48 million in revenue bonds, demonstrating that there is still a vibrant competitive marketplace. In the coming days, further projects from various states—including education and infrastructure funding—are also slated for pricing, hinting at a sustained supply chain that could keep investor attention piqued.

The municipal bonds market exhibits a confluence of encouraging investor sentiment, substantial pre-existing demand, and varied issuer dynamics. As supply predictions indicate a potential uptick, stakeholders must remain vigilant to navigate the complexities of a potentially evolving landscape. This alignment of market forces suggests that despite certain challenges, the demand for municipal bonds is poised to remain strong, offering opportunities for both issuers and investors alike.