The municipal bond market has been experiencing fluctuations influenced by various economic indicators, and recent developments indicate an uptick in activity. Traders and investors in the market are observing shifts prompted by changes in U.S. Treasury yields and equities. As municipalities gear up for increased issuances, a detailed exploration of these trends can provide valuable insights into both the immediate and future landscape of municipal securities.

The Current State of Munis and Treasury Yields

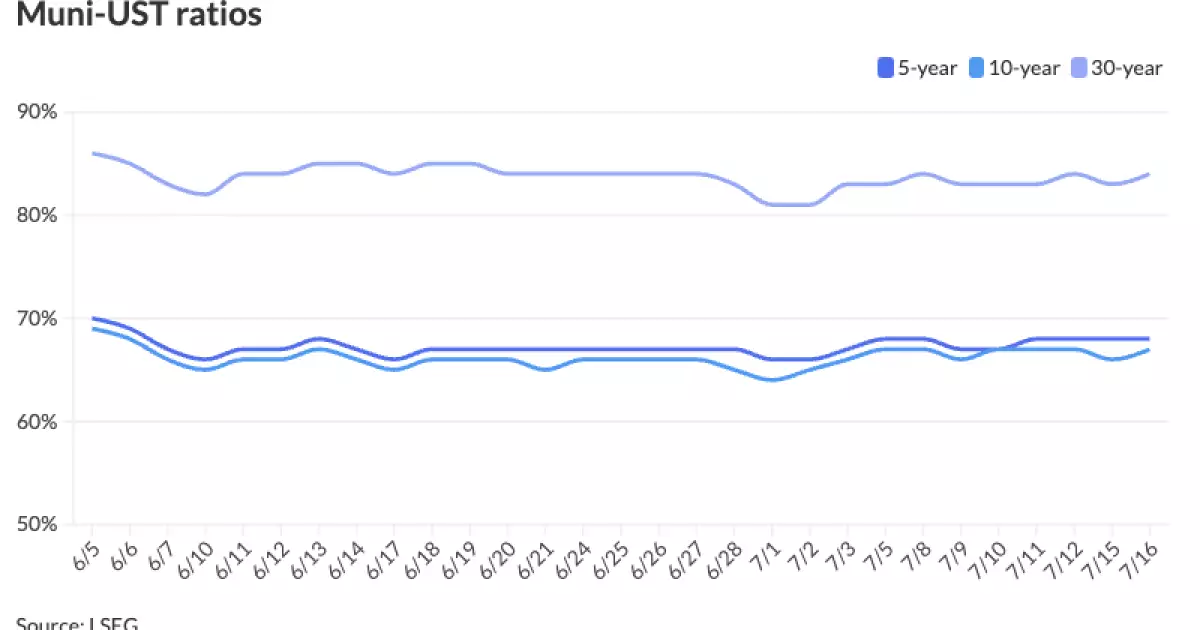

Recent trading sessions have shown a firming in municipal bonds, with the primary market gaining momentum. According to Refinitiv Municipal Market Data, the ratio of two-year munis to Treasuries stands at 65%. This ratio fluctuates across various maturities, with notable figures of 66% for the three-year, 68% for the five-year, 67% for the ten-year, and 84% for the thirty-year bonds. Furthermore, ICE Data Services has similarly reported these ratios, which serve as essential benchmarks for investors attempting to gauge the relative attractiveness of municipal bonds against U.S. Treasuries.

In a broader context, changes in interest rates set by the Federal Reserve and trends in consumer price indexes are influential factors that affect both municipal bonds and Treasuries. Recent comments from market analysts point to a market rally spurred by expectations for potential Federal Reserve rate cuts in the near future. This speculative optimism about monetary policy has resulted in increased investor interest in the municipal bond sector.

While shorter maturity bonds appear to be in demand due to their direct correlation with prospective Fed rate cuts, analysts caution against an overzealous approach. As highlighted by market analyst Matt Fabian, shorter-term maturities might currently be deemed “overbought.” This situation necessitates careful scrutiny and could suggest that yielding opportunities might lie outside of the immediate front-end maturities that typically attract naive momentum traders.

Contrastingly, the long-term segment of the yield curve remains relatively “oversold” according to Fabian’s analysis, which could open up considerable returns for discerning investors. The municipal market’s advantageous positioning relative to tax-advantaged yields not only entices returning retail investors but also signals the commencement of the reinvestment cycle, with forecasts estimating close to $40 billion in reinvestment for August—surpassing July and marking a significant opportunity for market participants.

As the current week progresses, the primary market is anticipating an estimated issuance of about $10.7 billion, reflecting a potential growth in market liquidity. Recent transactions have included significant bond offerings from various municipalities, such as the $921.86 million aviation revenue refunding bonds from Miami-Dade County, and additional projects from Georgia and Oregon entities.

These issuances are indicative of a robust pipeline despite some fluctuations in mutual fund flows, which have been recorded as inconsistent recently. Nevertheless, the growth in exchange-traded fund inflows may suggest that investors are holding cash reserves in anticipation of more strategic allocations. As summer transitions into fall, there’s a consensus among market insiders that the trend of thicker inventories will persist, allowing for advantageous opportunities as issuers look to capitalize on market conditions.

Looking ahead, traders can expect continued strong performance in the municipal bond sector. Analysts predict a sustained level of issuance as municipalities look to fund essential projects. With several large-scale bond offerings set to hit the market, including future tax-secured subordinate bonds from New York City and substantial general revenue bonds from the University of California, there are ample opportunities for investors.

Furthermore, the prevailing sentiment within the market indicates that the surge in supply, regardless of its magnitude, should not adversely impact overall performance. Particularly if market conditions can stabilize through positive fund flows, investors will likely find a conducive environment for tax-exempt allocations.

The municipal bond market is evidently poised for a critical period marked by opportunities driven by interest rate expectations and a robust issuance calendar. For investors, navigating this environment entails balancing the prospects of capitalizing on oversold bonds while remaining cautious about overly optimistic short-term investments. As the municipal bond landscape evolves, strategic allocation and informed decision-making will serve as essential tools for success in the coming months.