The municipal bond market experienced a mixed performance on Wednesday, with evident selling pressure on the short end due to few sizable deals pricing in the primary market. Despite this, munis have managed to hold relatively well as yields remain in a tight range. The AAA HG curve in the muni market has maintained stability in March, with most spots on the curve reaching or nearing year-to-date highs. J.P. Morgan strategists noted that absolute yields continue to be attractive given the trading range over the past three years and long-term projections for lower rates in the coming year. However, the recent underperformance of the muni HG curve relative to the broader fixed income market suggests that the market remains in a delicate balance.

Ratios such as the muni-to-Treasury ratio present an interesting insight into the market dynamics. The two-year ratio stood at 64%, the three-year at 64%, the five-year at 61%, the 10-year at 60%, and the 30-year at 84%, according to Refinitiv Municipal Market Data. These ratios offer a glimpse into the relative value of municipal bonds compared to US Treasuries. J.P. Morgan strategists pointed out that the 2yr IG municipal ratios have moved towards the middle range compared to taxable fixed-income, indicating pricing adjustments within the market.

The technical environment in the muni bond market plays a crucial role in shaping market trends. J.P. Morgan stated that current valuations and expectations for technicals suggest potential underperformance in the coming months, particularly in March and April. Ben Barber from Franklin Templeton had a more optimistic view, highlighting the strong supply and demand dynamics in the market. Barber emphasized that primary issuance is on the rise, with The Bond Buyer 30-day visible supply sitting at $7.61 billion. The anticipation of increased Build America Bond refundings could further boost issuance levels, provided that legal hurdles do not impede the process.

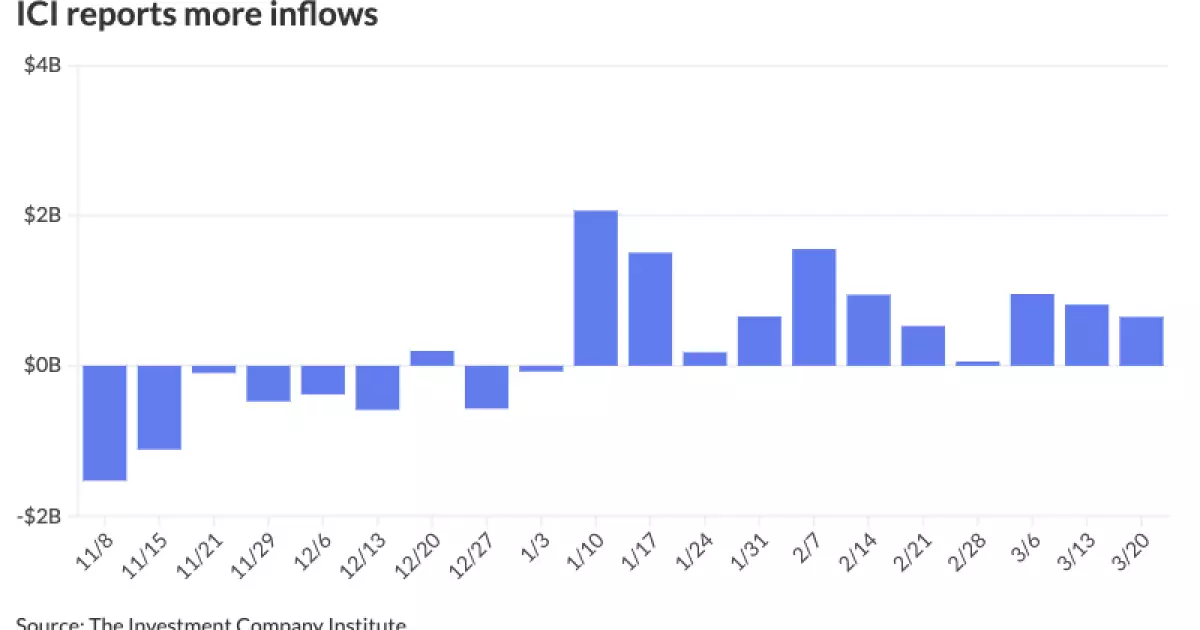

Market participants continue to exhibit strong demand for muni bonds, with oversubscription of deals being a common occurrence. Demand outpacing supply has been particularly evident in the separately managed account buyer base, indicating favorable conditions for issuers. The Investment Company Institute reported consistent inflows into municipal bond mutual funds for 11 straight weeks. Exchange-traded funds, however, saw outflows, suggesting a nuanced investor sentiment towards muni bonds. In the competitive market, the Santa Clara Unified School District successfully sold $148.360 million of 2024 GO refunding bonds to Morgan Stanley, showcasing continued investor interest in high-quality municipal issuances.

On the AAA yield curve front, there were fluctuations in yields across different maturities. Scales like Refinitiv MMD, ICE AAA, S&P Global Market Intelligence, and Bloomberg BVAL showed variations in yield levels for different maturity points. Treasuries, on the other hand, displayed a firmer performance, reflecting the broader dynamics in the financial markets.

The municipal bond market presents a nuanced landscape with various factors at play. While certain indicators point towards potential underperformance, strong demand, and consistent inflows suggest continued investor interest in municipal bonds. Monitoring technical developments and yield ratios will be crucial in gauging the market direction in the coming months.