The municipal bond market has once again demonstrated its resilience, a pivotal trait that investors heavily rely upon during times of financial unrest. Recent data reveals a slight firming in municipal bonds, a sign that the market is finding its footing after the tumultuous swings seen in the preceding weeks. With U.S. Treasury yields declining and equities experiencing a sell-off, there’s a sense of cautious optimism among fixed-income investors. Key metrics indicate a stabilization; for example, the two-year municipal bond yields have settled at around 80% of comparable U.S. Treasuries, suggesting a renewed competitive edge for municipal bonds despite the overarching market volatility.

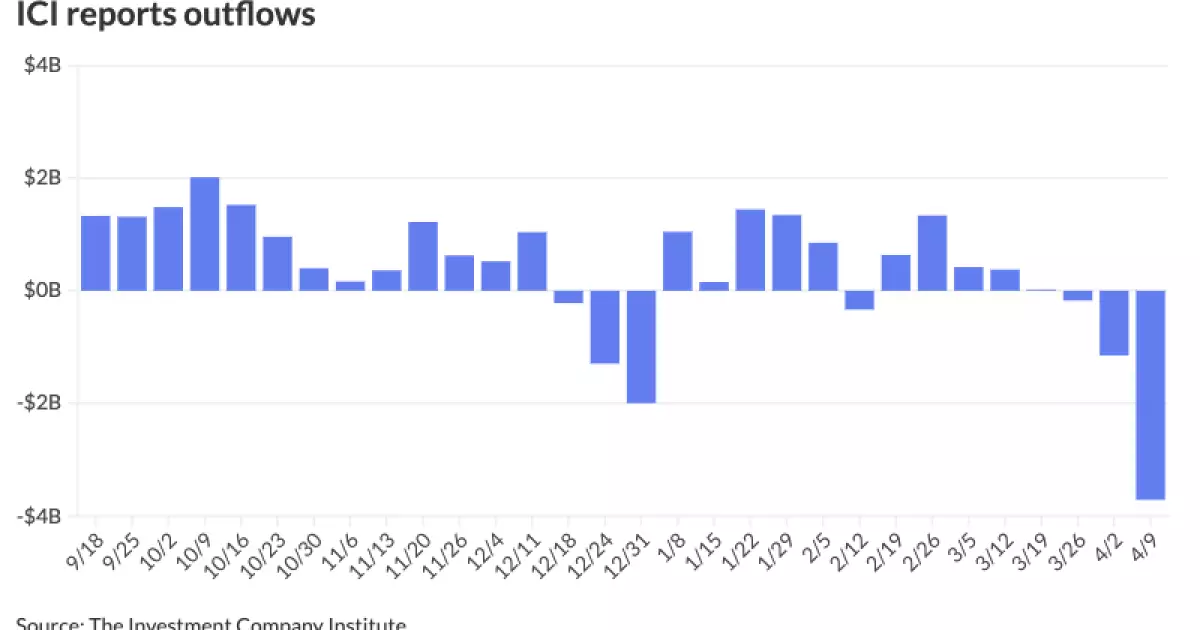

This positive trend begs the question: is this a fleeting moment of optimism, or is there something fundamentally shifting in the market dynamics? With the Investment Company Institute reporting significant outflows—$3.714 billion just for the week ending April 9—one might argue that cautiousness is warranted. Municipal bonds, often viewed as safe havens during economic uncertainty, are now facing a different challenge: the distribution of forthcoming bond supply amidst heightened investor scrutiny.

Market Activity and Investor Sentiment

Recent observations from key portfolio managers indicate that a robust lineup of competitive bond sales—from North Carolina’s limited obligations to Anne Arundel County’s general obligation bonds—has been met with enthusiasm from institutional buyers. The levels achieved during these sales underscore a reinvigorated appetite for bonds, particularly in the short and intermediate yields, which now sit close to their AAA reference points. The disparity in performance between this week’s competitive bonds and those from the previous week showcases a notable shift: instead of widespread concessions, there is now a tide favoring par or very minor concessions against the backdrop of investor confidence.

Moreover, Kim Olsan, a senior fixed-income portfolio manager, notes the emergence of a bidding pool stepping in to capitalize on yield discrepancies. This is a clear indicator that investors are keenly looking for opportunities amidst ongoing volatility, reflecting a market that, while still apprehensive, is willing to take calculated risks. It signals a potential end to the excessive conservatism that followed recent downturns.

The Changing Nature of Municipal Bond Transactions

What is particularly telling is how the structure of municipal bond transactions is evolving. There’s been a notable increase in dealer-to-customer business over inter-dealer volume, suggesting that more retail investors are participating in the market directly, rather than relying on institutional middlemen. This shift could be indicative of a broader trend where retail investors, equipped with more information and tools than ever before, are taking charge of their investment decisions.

The municipal bond market is also witnessing more elevated secondary trading volumes, emphasizing an environment ripe for volatility. With average daily par values from buyers reaching $12 billion—up from $10 billion last year—there’s tangible movement and activity that keeps the market dynamic. However, the strategic positioning by various issuers and their alignment to investor yield expectations can significantly influence the ability of upcoming offerings to lure in the necessary capital.

Yields and Value: Where Are We Headed?

In the current context, yields are observed to have receded significantly from the peaks earlier this month, with both ultra-short yields and longer-term rates adjusting in ways that stimulate dialogue among investors about fair value. The one-year AAA MMD yield, for example, recently traded at an annual high of 3.45%. Such movements will attract top-bracket buyers by generating tax-equivalent yields that cross the 5.00% threshold, a crucial psychological barrier for many tax-sensitive investors.

While there are undeniable benefits in the current pricing environment, including the enhancement of yields and ratios across various coupon types, concerns remain. For instance, high-grade bonds at the longer end of the curve have corrected by approximately 110 basis points, hinting at a broader recalibration that could create barriers for new entrants into the market. This is compounded by a slightly cautious atmosphere wherein funds are seeing more pronounced redemptions, particularly ahead of the April 15 tax deadline, an annual phenomenon that could exert additional pressure on liquidity.

With the municipal bond market continuing to adapt to the ebbs and flows of external pressure, it’s crucial for market participants to remain vigilant and informed. Investors should consider the intricate balance between opportunity and caution, leveraging the current positivity while preparing for possible fluctuations driven by external economic factors. Only through understanding and adeptly navigating these complexities can investors position themselves to capitalize on what remains a foundational component of their portfolios.