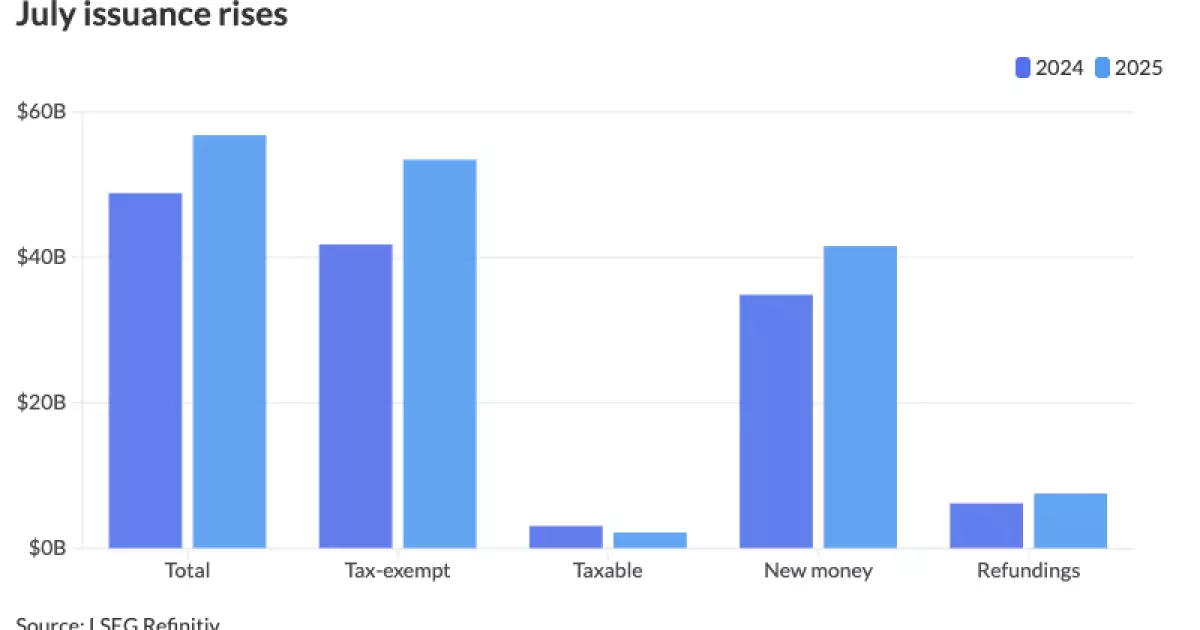

The first half of 2025 has defied expectations, witnessing an explosive increase in municipal bond issuance that could be mistaken for genuine economic vitality. With issuance surpassing $280 billion—an impressive 14.3% year-over-year increase—markets appear robust. Yet, beneath this frenetic activity lies a complex web of strategic frontloading, political anxieties, and a distorted perception of fiscal health. While many investors celebrate record volumes and soaring state-level borrowing, such euphoria risks masking underlying vulnerabilities that could threaten long-term stability.

This relentless issuance spree is driven by issuers eager to lock in low-cost capital amid anticipations of policy shifts. Concerns about potential tax exemption reforms or funding cuts for sectors like higher education and healthcare spurred a rush to market. As a result, many political entities and institutions frontloaded their debt deals, trying to preempt any legislative or legislative-related upheavals. While this strategy may have provided short-term relief, it also artificially inflates the market’s growth figures, creating the illusion of a thriving economy when, in reality, it might just be a bubble inflated by panic.

Furthermore, this surge coincides with a higher interest rate environment, boosting the immediate appeal of new issuances for yield-starved investors. The ability to garner an additional 30 to 40 basis points per month seems like a boon, yet it also exacerbates the risk of over-leverage. As market participants chase volume and yield, careful scrutiny of creditworthiness and sustainability often gets sidestepped. The danger lies in mistaking activity for health—believing that high issuance volume equates to fiscal resilience rather than recognizing it as a sign of hurried borrowing with potentially shaky foundations.

Distorted Market Dynamics and the Illusion of Stability

The pattern of aggressive issuance has significantly distorted the traditional cycle of municipal markets. Historically, issuance peaks gradually as markets stabilize, but this year, the momentum carried from 2024 persisted into early 2025 with remarkable consistency. Investment banks and issuers alike aimed to “get deals done,” often hurriedly pricing deals as market conditions appeared temporarily favorable. The result? Record-breaking weekly issuance volumes that look impressive but may be unsustainable in the long run.

This kind of market behavior fosters a sense of invincibility, leading many to believe that the muni space is resilient. However, the underlying fundamentals—especially in sectors like healthcare, education, and infrastructure—remain precarious. Many of these bonds financed programs vulnerable to political whims or macroeconomic shifts. The willingness of prestigious universities to reissue bonds amid recent funding freezes underscores a phenomenon: entities with strong reputations are leveraging the current liquidity environment to shore up finances, possibly at the expense of future flexibility.

The rapid rise in issuance also has implications for credit quality. When issuers rush to market to capitalise on market conditions, due diligence may suffer. Bond ratings, once reflective of robust financial health, could be more prone to overestimation. If market conditions suddenly turn negative—as they inevitably do—the fallout could be severe. The avalanche of new debt may find itself under scrutiny, with weaker credits facing distress, and the entire market potentially destabilized by a sudden correction.

Political and Policy Risks: A House of Cards?

While recent legislation seemed to preserve the core tax exemptions—temporarily alleviating fears of a fundamental overhaul—the political landscape remains unpredictable. Historically, every election cycle rekindles anxiety over the fate of tax benefits. The current environment is no different. Although the latest budget bill left exemptions intact, this is no guarantee for the future, especially considering how targeted private-activity bonds and specialized sectors remain politically contentious.

This persistent uncertainty fuels a strategy of preemptive issuance, which, while logical in the short term, could deepen vulnerabilities. Many local governments and institutions are now heavily leveraged, banking on continued political support and stable tax policies. Any future threat to these exemptions or to the federal funding streams—whether through partisan shifts or broader macroeconomic adjustments—could trigger liquidity strains or defaults that ripple across the municipal landscape. The recent increase in debt issuance by wealthy states like California and Texas might appear impressive but comes with the caveat that over-leverage can lead to fiscal indigestion if growth slows or policies change.

The risk is compounded by the fact that the market seems complacent. Despite volatility earlier this year due to tariffs and macro shocks, market participants remained active. This could be a sign of overconfidence; however, history suggests that complacency in finance often precedes a correction. The question is whether today’s elevated issuance signals genuine strength or a temporary illusion that masks risk accumulation.

The Dilemma of Overreliance on Heavy Borrowing

At the core of this discussion lies a difficult truth: municipal markets are increasingly dependent on heavy borrowing to maintain their momentum. States and institutions are borrowing more than ever, with California leading the charge at over $45 billion year-to-date. While such figures appear impressive, they prompt a critical question—are these debts truly sustainable?

The short-term benefits of borrowing—funding necessary infrastructure, maintaining public services, and investing in growth—must be balanced against the long-term costs. Excessive reliance on debt can create a hidden burden for future generations, especially if tax revenues fail to meet projections or if economic growth stagnates. When a state or government becomes overly leveraged, its capacity to respond to future crises diminishes drastically, and even the strongest issuers are not immune from fiscal decline.

In an environment where the market rewards volume over value, investors must scrutinize beyond headline stats. The risk of underestimating the potential for credit deterioration is high, especially if the conservative assumptions that currently underpin ratings prove tenuous in the face of economic shocks. As the market continues to “fix” its supply-demand imbalance through record issuance, it risks sowing the seeds of a deeper correction hidden beneath the surface of apparent prosperity.

—

Note to Readers: While the current municipal bond market displays a picture of resilience, beneath this veneer lies a fragile structure built on aggressive issuance, political uncertainty, and over-leverage. If policymakers and investors fail to recognize these underlying risks, the coming months might reveal a much less optimistic reality.