Investors in the municipal bond market have been focused on the primary market this past week, as the secondary market has taken a backseat. With up to $13 billion of supply on tap, there is ample opportunity to buy paper, according to experts like Chris Brigati from SWBC and Anders S. Persson and Daniel J. Close from Nuveen. The rise in issuance has kept muni yields elevated, but large new-issue deals are expected to be well received, especially by institutional municipal money managers.

In the primary market, there were several notable deals this week. From the Los Angeles Unified School District to the New Jersey Housing and Mortgage Finance Agency, a variety of bonds were priced with different terms and yields. Prices ranged from 3.50% to 4.7%, depending on the issuer and the terms of the bonds. Overall, the primary market remains active, with demand for well-structured credits.

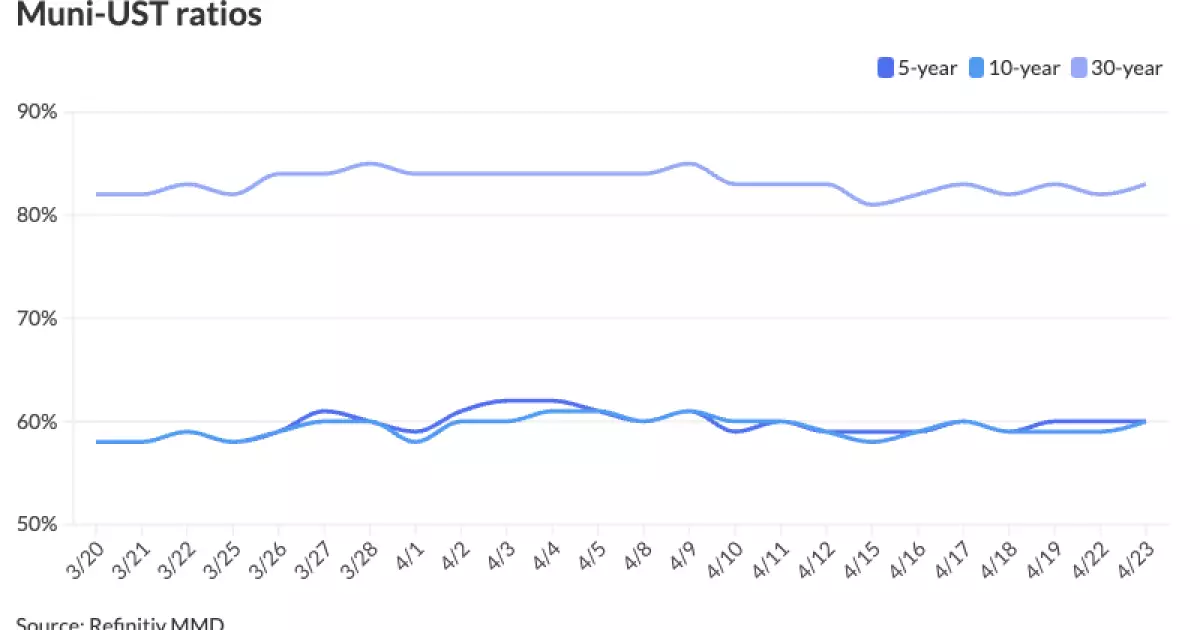

Muni-to-Treasury ratios have remained on the rich side, according to Refinitiv Municipal Market Data and ICE Data Services. Front-end yields have held up well, while term spreads have widened. There is a bifurcation in demand, with separately managed accounts and retail investors showing strength in the market. As the market looks towards potential Build America Bond refundings, there are opportunities for income-biased buyers, especially for structured credits just outside typical retail buying ranges.

Despite the strength in the front end of the curve, the back end has not been well supported, especially with May being the worst reinvestment month of the year. Near-term optimism is hard to come by, but well-structured credits are still seeing strong demand. As the tax deadline passes and investors refocus on the market, opportunities may arise for buyers looking for quality yields on the long end.

Upcoming Deals and Competitive Market

Looking ahead, there are several deals set to price in the coming days, from Brightline Florida Passenger Rail Project bonds to health care revenue bonds and school building bonds. The competitive market also remains active, with entities like Denton County, Texas, and the Florida Department of Transportation selling bonds at competitive rates.

The municipal bond market continues to see activity in the primary market with a focus on new-issue deals. Despite challenges in the back end of the curve, there are opportunities for income-biased buyers and investors seeking quality yields. As the market evolves and new deals come to market, investors will need to be strategic in their approach to navigating the changing landscape of the municipal bond market.