As the week came to a close, municipal bonds experienced some weakness in certain areas, particularly as larger issues were priced. Despite this, municipal bond mutual fund flows indicated that retail investors were actively engaged, and high-yield bonds continued to outperform the broader investment-grade market. U.S. Treasuries faced pressure due to economic data and Federal Reserve commentary, sparking concerns about inflation expectations and potential rate cuts. Equities ended the session in the red, reflecting broader market unease.

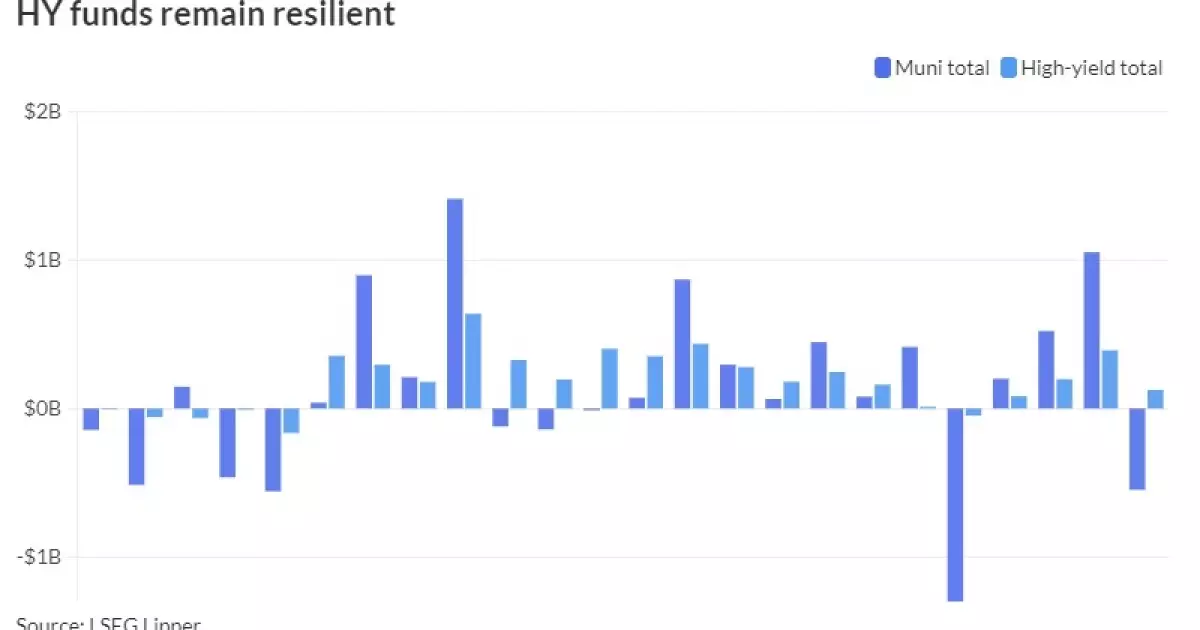

Triple-A yields saw an increase of one to two basis points, while Treasury yields climbed as much as six basis points on the short end by the close of trading. The muni-to-Treasury ratio on Thursday stood at varying percentages across different maturity levels. Municipal bond mutual funds experienced outflows totaling $548 million, while high-yield funds saw inflows of $125 million. Retail investors showed strong interest in high-yield bonds, with J.P. Morgan noting that high-yield funds exhibited resilience compared to investment-grade funds, which saw outflows of $673 million.

Weekly municipal fund outflows were primarily driven by open-end funds, offset partially by inflows into exchange-traded funds. The increasing popularity of ETFs among retail investors has been crucial in driving market activity and boosting confidence. Municipal bonds faced slight weakness on Thursday, but the performance relative to the UST rally on the previous day was expected given the level of issuance and prevailing relative values in the market. The market’s visible supply stood at $16.55 billion, signaling the availability of a range of credits for investors.

Credit Quality and Value

Notably, wider credit spreads and a surge in the calendar have enhanced the value proposition for investors, effectively placing a significant portion of the market on sale. This phenomenon has benefited high-yield bonds, which have outperformed due to strong demand and reactive secondary flows. The widening credit spreads have been evident across the credit spectrum, with high demand for New York credits that are pricing at attractive levels. Customer buying volume has been substantial in certain maturity buckets, indicating favorable allocations based on yield considerations.

Yield Curve Trends

Refinitiv MMD’s scale showed minor adjustments in yields across different maturities, with incremental changes in the one-year, two-year, and five-year segments. Similarly, the ICE AAA yield curve remained relatively stable, with unchanged yields in several maturity points. The S&P Global Market Intelligence municipal curve and Bloomberg BVAL also saw limited changes in yields, reflecting the overall stability in the market. Meanwhile, Treasuries experienced weakness, with varying yield movements along different maturity points as the trading day concluded.

The municipal bond market continues to exhibit dynamic trends driven by investor behavior, economic indicators, and Federal Reserve actions. Retail engagement, credit quality considerations, and yield dynamics are key factors influencing market performance and investor decision-making. As market conditions evolve, it is essential for investors to stay informed and adapt their strategies accordingly to navigate the ever-changing landscape of municipal bond investing.