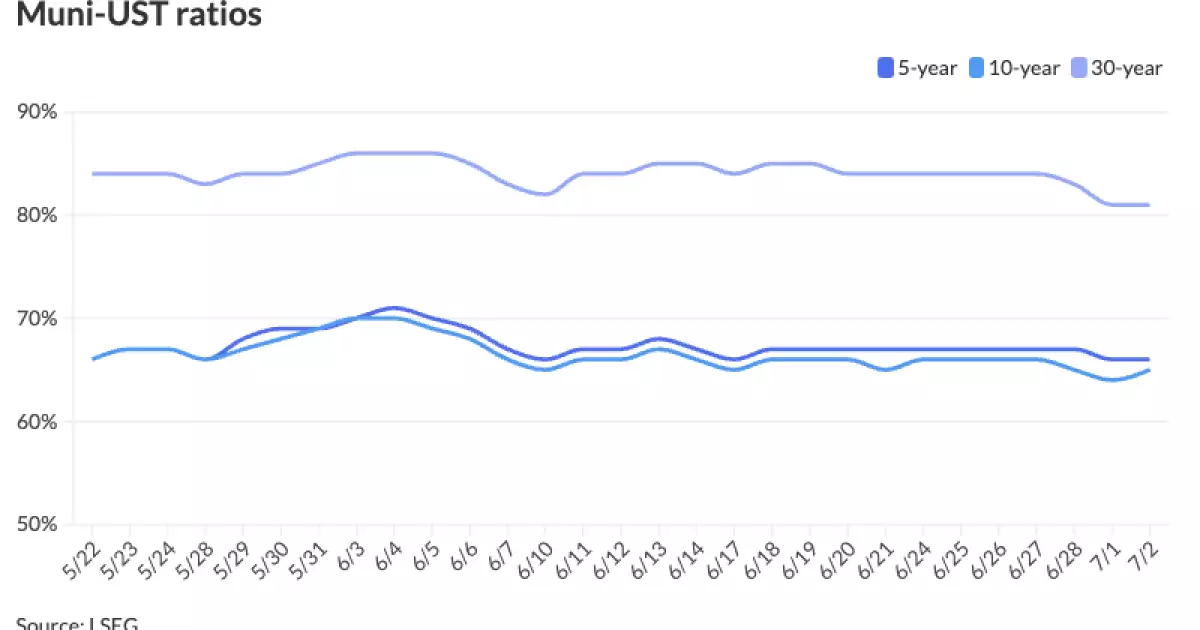

The municipal market in the US remained steady this past week as U.S. Treasury yields experienced a decline while equities registered an increase. Industry experts are predicting slow activity in the market this week due to the usual trend of issuers taking a break during holiday-shortened weeks. This is expected to result in a “muted” new-issue calendar, with secondary market activity also anticipated to be light. However, things might change as around $31 billion of July reinvestment cash is set to enter the market early this week, offering a prime opportunity for investors to put their cash to work. There is a consensus among experts that with the absence of new issuances and a surplus of dealer balance sheets, the municipal market could become more aggressive in the coming weeks. This shift in dynamics might be attributed to the current muni-to-Treasury ratios, which are in the mid-60s, as noted by David Litvack from BofA Securities.

According to Refintiv Municipal Market Data, the muni-to-Treasury ratios were as follows on Tuesday: two-year at 65%, three-year at 65%, five-year at 66%, 10-year at 65%, and 30-year at 81%. On the other hand, ICE Data Services reported slightly different ratios, with the two-year at 66%, three-year at 66%, five-year at 66%, 10-year at 65%, and 30-year at 81%. Litvack pointed out that while valuations have increased in June, they have not reached the levels observed at the beginning of the year. He expects these ratios to remain elevated throughout the summer as issuance slows down from the highs observed earlier in the year.

Looking back at the month of June, tax-exempt munis rallied alongside USTs, outperforming due to strong reinvestment and attractive muni-to-UST ratios. This resulted in a negative 3 muni-UST ratio of outperformance, leading to fair-to-rich valuations across the market. The Bloomberg Municipal Index posted a total return of 1.53% in June, with year-to-date returns standing at -0.40%. Munis outperformed the U.S. Treasury Index, which returned 1.0% during the same period. The MMD-UST five-, 10-, and 30-year ratios all saw declines, ending the month at 67%, 65%, and 83%, respectively. June witnessed an increase in issuance volume, driven by improved market momentum and the growth of Build America Bond refundings. Fund flows for the month were slightly positive despite some outflows, mainly due to inflows into high-yield and long-term funds.

In terms of AAA scales, Refinitiv MMD, ICE, S&P Global Market Intelligence, and Bloomberg BVAL all reported similar figures for various maturities. The one-year, two-year, five-year, 10-year, and 30-year yields remained relatively stable across different scales. Treasuries experienced a firmer trend overall, with yields showing a downward trajectory across the board. This in turn might have an impact on the municipal market as investors assess the potential returns and risks associated with different asset classes.

The municipal market in the US is expected to witness a period of relative calm in the coming weeks, with a focus on reinvestment cash and subdued issuance activity. The dynamics of muni-to-Treasury ratios and market valuations will play a crucial role in shaping investor sentiment and behavior. It will be interesting to see how market participants navigate through these evolving conditions and capitalize on the opportunities presented by shifting market trends.