The municipal bond market experienced slight weakness in secondary trading on Wednesday, with a particular focus on the Los Angeles Unified School District’s nearly $3 billion pricing for institutions. The rise in U.S. Treasury yields and mixed performances in equities also contributed to the market dynamics. Despite this, GW&K Investment Management strategists noted that munis began the second quarter in excellent shape, with credit spreads at fair value and muni-UST ratios starting to cheapen. This implies a favorable market condition for investors seeking opportunities in the municipal bond space.

When looking at the muni-to-Treasury ratios, different sources provided slightly different numbers, but the overall trend indicates that certain parts of the curve present attractive opportunities. J.P. Morgan strategists highlighted that the longer end of the tax-exempt market offers the most value, with 30-year AA tax-exempts firmly positioned within the range of the past three years. This suggests that investors might find value in the longer duration bonds, especially given the current market conditions.

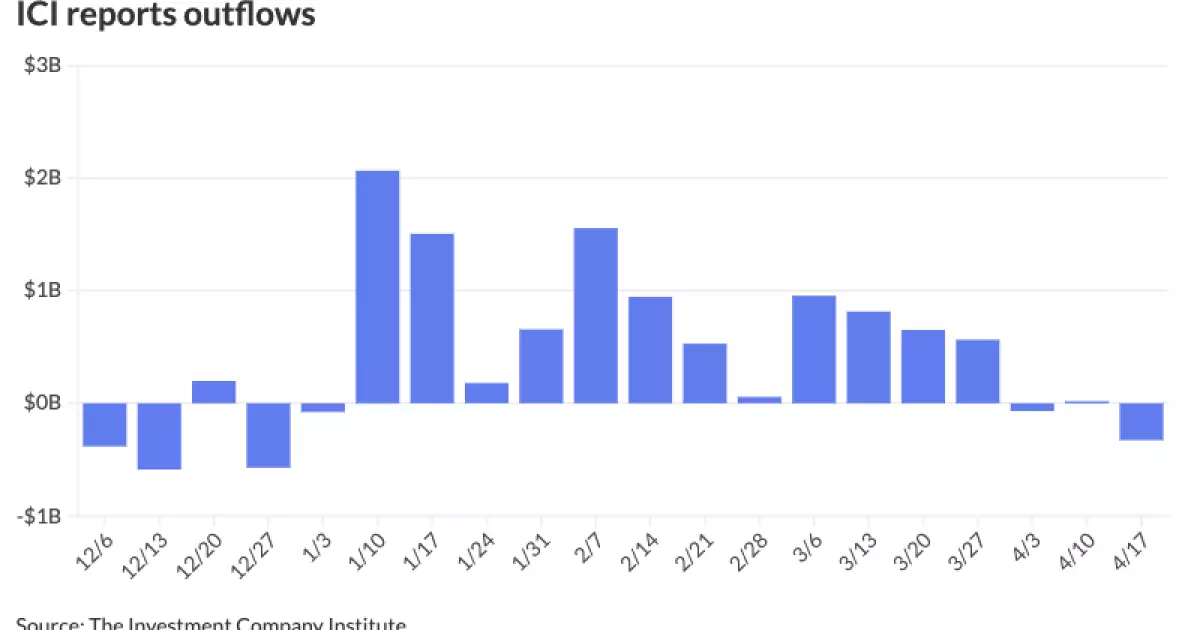

Despite concerns about expensive valuations, supply surges, and low reinvestment demand, there has been consistent investor appetite for tax-exempts throughout the quarter. As election campaigns gain traction, retail investors are being encouraged to lock in muni yields to potentially benefit from future tax rate changes. This sentiment is expected to bring stability to the market and counteract any volatility stemming from data-driven decisions by the Federal Reserve.

In the primary market, several institutional pricing deals were observed, including the Los Angeles Unified School District’s GO refunding bonds, Series A. Other issuers like the New Jersey Health Care Facilities Financing Authority, the Maine Municipal Bond Bank, and Denton County, Texas, also tapped the market for funding. These deals reflect the ongoing demand for municipal bonds from both issuers and investors, signaling a continued interest in the asset class.

The pricing details of various bonds indicate the diverse nature of the municipal bond market, with different issuers offering bonds across various terms and yields. BofA Securities, Jefferies, and other underwriters were actively involved in pricing bonds for different projects and entities. The ratings assigned to these bonds reflect the creditworthiness of the issuers and provide investors with insights into the risk associated with these investments.

As the market continues to evolve, it is essential for investors to stay updated on the latest developments and trends in the municipal bond space. The changing interest rate environment, economic conditions, and policy decisions can all impact the performance of municipal bonds. By staying informed and conducting thorough analysis, investors can make well-informed decisions regarding their bond portfolios and capitalize on opportunities presented in the market.

Overall, the municipal bond market offers a wide range of opportunities for investors seeking tax-exempt income and diversification within their portfolios. By carefully analyzing market dynamics, yield ratios, investor sentiment, and primary market activity, investors can navigate the municipal bond market effectively and make informed investment decisions.