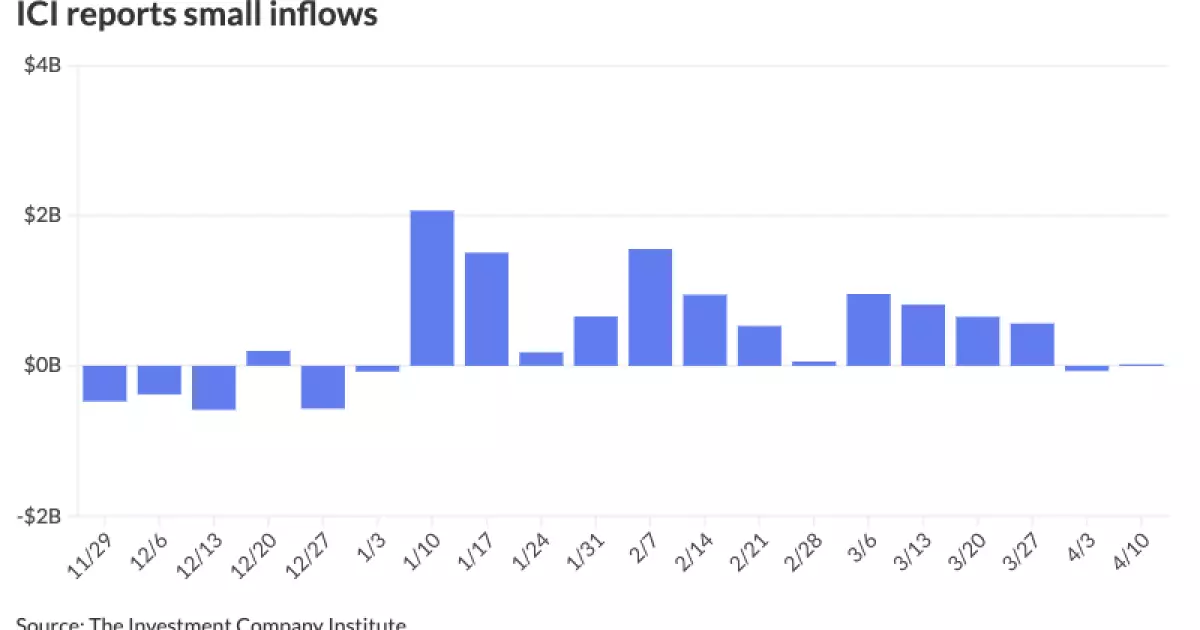

The municipal bond market experienced little change on Wednesday as the supply of bonds slowed down and small inflows into muni mutual funds returned. This shift occurred amidst falling U.S. Treasury yields and losses in the equities market. The Investment Company Institute reported a slight increase in municipal bond mutual funds for the week ending April 10, with investors adding $18 million to funds after seeing $69 million of outflows in the previous week. Additionally, exchange-traded funds saw inflows of $944 million, following $19 million of outflows the week prior.

Market Commentary

J.P. Morgan strategists noted that the yield in all spots on the muni AAA HG curve hit new year-to-date highs, with the muni HG curve showing outperformance compared to the broader fixed income market this month. They mentioned that the rapid UST volatility is impacting muni yield movements, although it hasn’t affected the strength of the new-issue market. According to Jeff Timlin, a managing partner at Sage Advisory, absolute yields remain attractive given the trading range over the past three years and long-term projections for lower rates this year.

Despite some richening last week, the two-year investment-grade muni ratios compared to taxable fixed-income are at transactional levels. Specifically, ratios become progressively richer when moving into the five- to 10-year part of the curve, with the 10-year spot remaining more attractive in taxables versus tax-exempts. The two-year muni-to-Treasury ratio sat at 64%, the three-year at 63%, the five-year at 60%, the 10-year at 60%, and the 30-year at 83% according to Refinitiv Municipal Market Data.

Technical Environment

J.P. Morgan strategists pointed out that current valuations and expectations for technicals suggest underperformance in the less favorable technical environment in April. They anticipate a softer period ahead, as there is expected supply coming until the beginning of June concerning the amount of money that needs to be reinvested through maturity coupon payments. This softness in the market presents a good entry point for investors looking to redeploy capital.

Visible Supply and Reinvestment

As of now, Bond Buyer 30-day visible supply stands at $8.93 billion. Reinvestment dollars are projected to pick up starting in June and running through August, traditionally the heaviest three-month period of maturity and coupon payments that require reinvestment.

AAA Scales

Various sources such as Refinitiv MMD, ICE AAA yield curve, S&P Global Market Intelligence, and Bloomberg BVAL reported different scales for AAA municipal bonds. The one-year was at 3.38%, and two years at 3.15% in Refinitiv MMD, while the ICE AAA yield curve showed 3.37% in 2025 and 3.17% in 2026. Differences were also seen in scales for the five-year, 10-year, and 30-year bonds across these sources.

Several entities are set to price bonds on Thursday, including the Arizona Board of Regents, the Washington State Housing Finance Commission, the Oklahoma Capital Improvement Authority, the Oregon Department of Administrative Services, and Wake County, North Carolina. Additionally, Albuquerque, New Mexico, and the Clark County School District in Nevada are scheduled to sell bonds via a competitive process.

While the municipal bond market may be experiencing some volatility and uncertainties, strategic opportunities exist for investors to navigate these challenges and find value in the current market environment. By closely monitoring trends, ratios, and upcoming bond offerings, investors can make informed decisions to optimize their portfolios in the municipal bond market.