The landscape of municipal bonds and related mutual funds is currently marked by paradoxical trends and fluctuating dynamics. Investors are witnessing a complex interplay of capital flows, regulatory influences, and seasonal effects, creating an environment ripe for analysis. This article unpacks these developments, highlighting the recent trends in mutual fund outflows and the implications for municipal bond performance heading into the new year.

On a recent Thursday, municipal bonds exhibited minimal changes alongside U.S. Treasuries while equity markets showed gains. This stability amidst an upturn in equities poses several questions about investor sentiment and the underlying regression in municipal bonds. Jeff Timlin, managing partner at Sage Advisory, characterizes the current market as experiencing a “seasonal winter softness.” This sentiment resonates in the trading patterns observed, as deficient staffing and reduced issuance weigh on market activity.

The term “seasonal winter softness” aptly captures the essence of this period, driven by factors such as median trading volumes and pricing anomalies. Investors, facing impending year-end transactions, are influenced by tax-loss selling, which can heighten market volatility and widen bid-ask spreads. This environment underscores the necessity for investors to navigate carefully through the eventualities of late-year financial maneuvers.

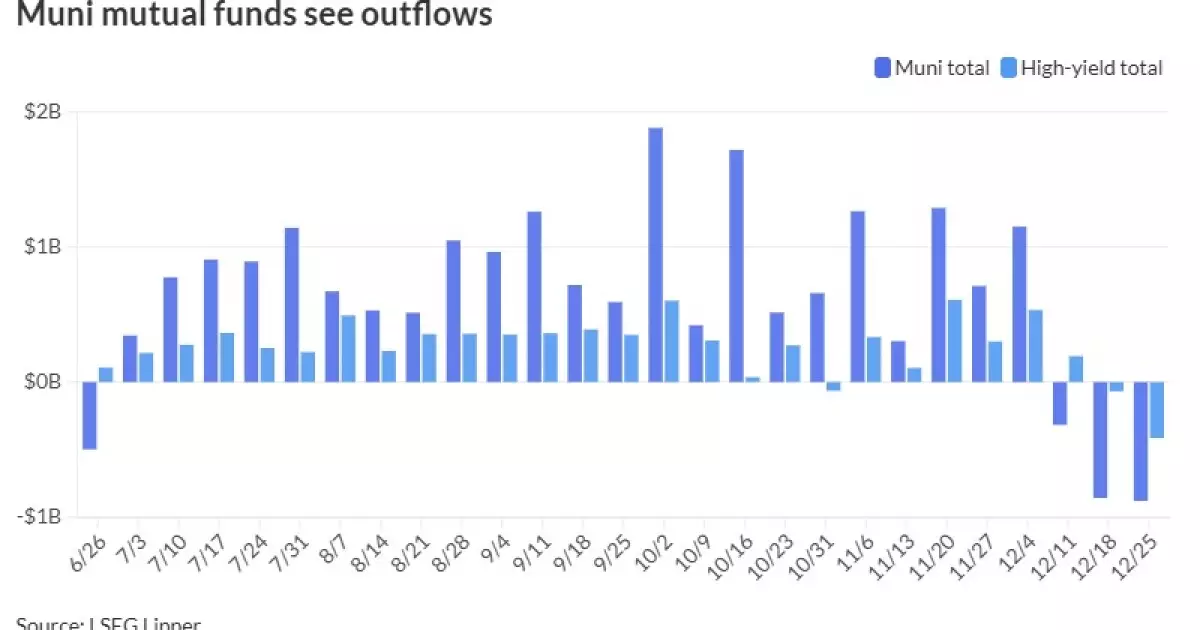

The trend of mutual fund outflows has become a prominent narrative, as evidenced by reports from LSEG Lipper indicating a withdrawal of $878.5 million from municipal bond funds in the week ending December 25. This follows an already significant outflow of $859.6 million in the previous week, painting a disconcerting picture of investor confidence. High-yield funds were not immune, suffering $413.6 million in outflows compared to just $71 million the week prior.

Moreover, discrepancies in reporting from LSEG Lipper compared to the Investment Company Institute (ICI) complicate the narrative further. The ICI recorded $222 million in outflows for the previous week, a stark contrast to the prior week’s substantial inflows of $1.04 billion. This situation signifies an evolving landscape where mutual funds face headwinds, raising critical questions about liquidity and future demand within the sector.

Conversely, money market funds are seeing a resurgence, reported to have achieved inflows of $1.477 billion in the week ending December 24. This is particularly notable against the backdrop of a previous week’s outflows that totaled $3.245 billion. The total assets in tax-exempt municipal money market funds rose to $133.17 billion, showcasing a significant recovery.

The average yield on these funds has also increased, now sitting at 3.08%, a notable rise from the 2.49% recorded the previous week. Taxable money-fund assets mirrored this recovery trend, with over $53 billion added following substantial outflows prior. This indicates a reallocation of investor assets toward what is perceived as a more stable and profitable avenue during tumultuous market conditions.

As we approach the closing of the financial year, the market typically experiences a crunch due to the heavy flow of funds from maturities and coupon payments that necessitate reinvestment. Timlin has emphasized that the lack of new issuance during this period means that market movement will primarily hinge on secondary supply and existing dealer inventories. This scenario creates a predictive cycle of “rinse and repeat,” where broker liquidity and patience dictate market behavior.

Looking ahead to January, Timlin anticipates a return to more vigorous trading activities as fresh inflows drive a systemic shift in pricing strategies. The prospect of a potential $500 billion issuance is expected to be absorbed positively by the market, indicating optimism among investors despite preceding volatility.

Against this backdrop, the environment for municipal bonds appears cautiously optimistic. While immediate risks remain, including observed discrepancies in mutual fund reporting and fluctuating outflows, underlying market fundamentals indicate resilience. The current period of volatility is likely to be moderate, with cash reserves poised for deployment as opportunities arise.

Technicals should improve in the new year, suggesting a stabilizing effect on municipal bond values. The current ratios of municipal to U.S. Treasury yields further reflect a nuanced perspective: such valuations trait variability across different maturities signals potential for reclaiming fairer valuations as we transition into 2025. Hence, while challenges prevail in the short term, a more favorable investment landscape seems ripe for exploration in the coming months.