The municipal bond market is experiencing its own brand of turbulence in the wake of recent election outcomes and shifting monetary policies. As market participants seek to navigate this fluctuating environment, it is essential to dissect the current state of the municipal bonds, particularly in relation to U.S. Treasuries, to understand key trends that might shape the market’s short-term future.

As of Thursday, municipal yields were slightly varied, reflecting a mixture of losses at the shorter end of the yield curve and gains further out. Analysts described a week characterized by relative calm following the volatility that erupted after the elections. However, this period of tranquility may be deceptive, as strategists from firms like BlackRock suggest that volatility may persist as investors digest the implications of the elections alongside shifting Federal Reserve policies.

The municipal bond market typically enjoys robust support during the latter part of the year due to seasonal trends and diminishing new issues. Recent assessments indicate that issuance may decline, which could lend additional strength to the munis as demand persists in a market marked by uncertainty. This sentiment is reinforced by a comparison to similar fluctuations witnessed in November 2016, when municipal yields saw increases ranging from 50 to 70 basis points.

Moreover, fixed-income portfolio managers have noted that the yield landscape, particularly for bonds maturing between 2026 and 2032, lacks robust 3.00% handles. With a significant portion—around 16%—of the total secondary tax-exempt volume transacted within this range last week, any yield adjustments could directly influence municipal investment flows.

The dynamics between municipal securities and U.S. Treasuries have also highlighted a shift in ratios, suggesting potential opportunities for investors. For instance, following a 30-basis-point correction in two-year U.S. Treasury yields, notable declines in municipal-to-Treasury ratios were observed, settling around 60% for two-year municipals. This reduction indicates a relative decrease in the attractiveness of munis compared to Treasuries, especially for shorter maturities.

This phenomenon brings forth the notion that although munis may appear less favorable on a comparative basis, the balance across the yield curve still offers competitive options. Sections of the curve with yields above 3.00% demonstrate compelling potential, particularly for investors seeking steady defensive strategies. For instance, pre-refunded bonds scheduled to mature in 2025 are retaining their yields around this crucial threshold.

Yet, the anticipated increase in supply towards the end of 2024 poses a challenge, as it generates apprehension among potential buyers who are wary of what increased supply could mean for yields.

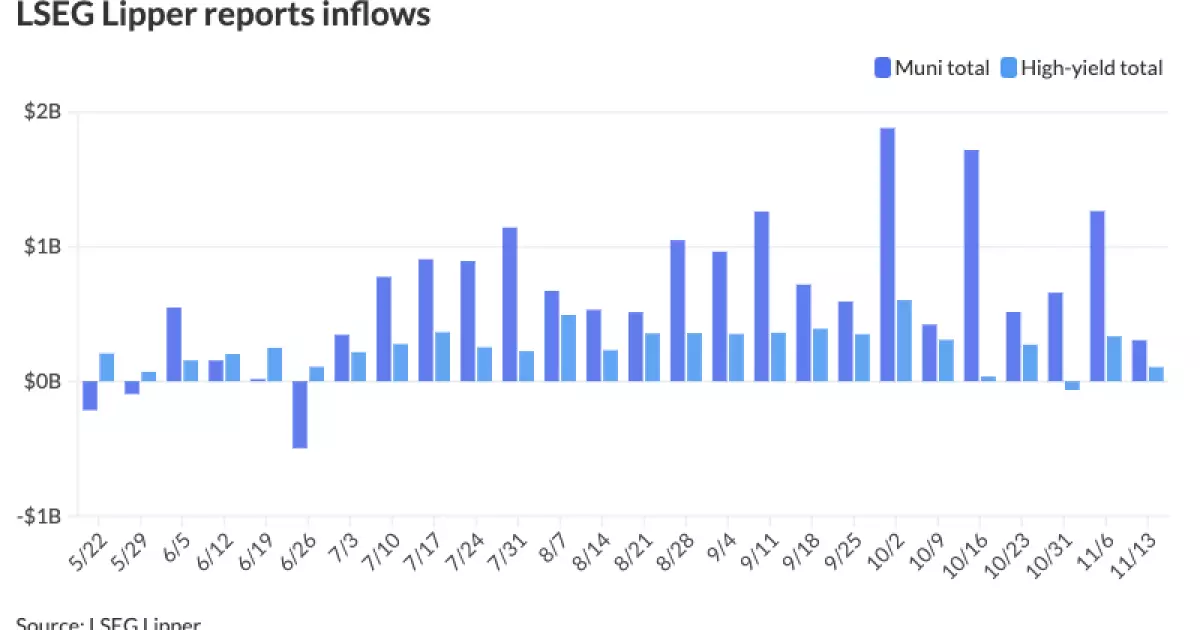

An essential element to consider in this volatile market is the ongoing movement in fund flows. Recent reports have shown a mixture of inflows and outflows into municipal bond mutual funds, with net inflows of $305 million reported, though trailing behind the previous week’s higher figures. This showcases an ongoing interest among investors, even as concerns about rate volatility linger.

However, the notable rise in inflows for high-yield funds, contrasted with recent outflows, underscores a broader shift in investment appetites as circumstances evolve. Investors appear to be navigating away from higher risks in search of more stable returns, which could lend additional pressure on yields moving forward.

Primary market activity has remained robust despite the ongoing volatility. Large bond issuances, such as those from Los Angeles and Omaha’s public utility divisions, have exhibited relatively strong pricing even as interest rates demonstrate mixed behavior. Competitive yields, particularly for longer-dated bonds, indicate that issuer credit ratings and associated risks are crucial factors influencing investor decisions.

As market conditions develop, it is critical for both issuers and investors to monitor daily bid lists and upcoming issuances, as these factors will heavily influence the supply-demand equilibrium. Historical trends in November and December indicate that new issuances could soar, presenting both opportunities and potential challenges for market participants.

Ultimately, the municipal bond market is navigating a complex landscape marked by recent electoral outcomes and anticipated changes in federal monetary policy. While the potential for heightened volatility lingers, municipal bonds also present an array of opportunities for astute investors who can monitor the evolving dynamics of the market. As we approach the end of the year, the interplay between issuance trends, yield ratios, and investor sentiment will critically shape the trajectory of municipal bonds in the foreseeable future.