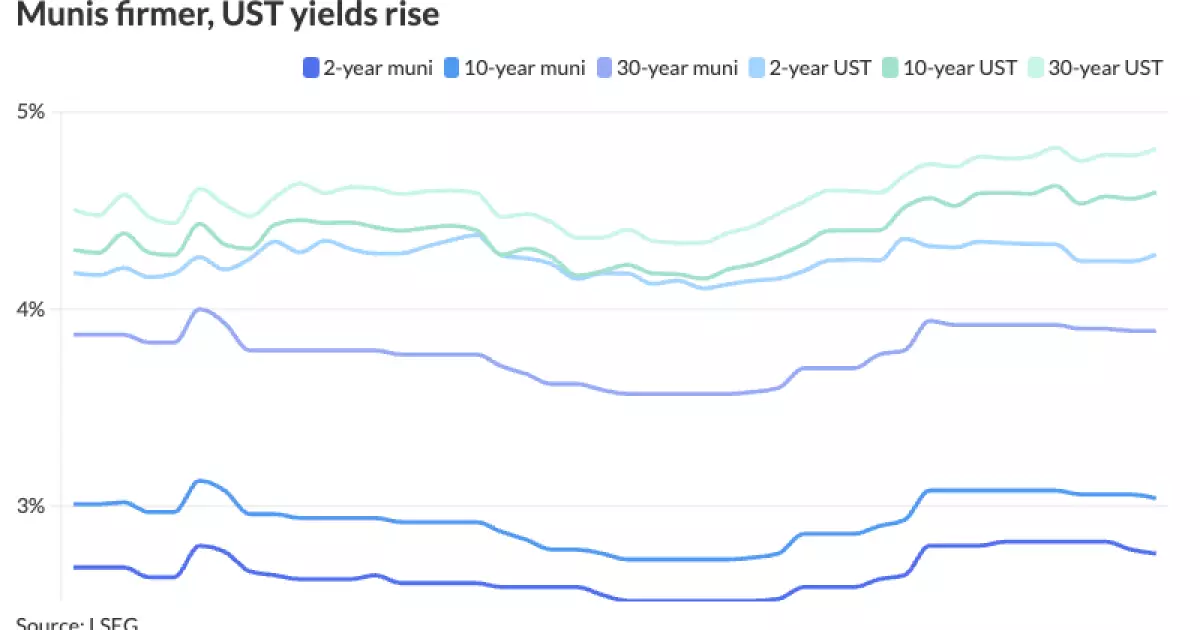

As the municipal bond market enters the first full week of the New Year, various developments are shaping investor sentiment. On the final trading day ahead of this exciting week, municipal bonds exhibited firmness amidst a landscape where U.S. Treasuries experienced slight declines. The anticipated influx of over $5 billion in new issue supply is set to further shape the market dynamics. According to recent data, yields on Triple-A rated bonds have decreased by up to seven basis points, particularly on one-year maturities. In contrast, U.S. Treasury yields edged up across various maturities, rising between two to four basis points.

Market analysts are beginning to shift their outlook as municipal bond yields reached attractive levels, inciting a resurgence of investor interest. Mikhail Foux, managing director at Barclays, noted that although January’s performance had been met with some skepticism, the subdued supply forecast suggests a potentially more favorable scenario for the upcoming weeks. With crucial economic data releases on the horizon, in addition to the January Federal Open Market Committee meeting, many issuers may opt to proceed cautiously, further affecting supply levels.

Analyzing Supply and Demand

The municipal supply landscape poses a key area of interest for investors, with the Bond Buyer reporting a visible supply totaling approximately $9.95 billion. This week, investors will be inundated with new issues, with a spotlight on a significant $1 billion offering from the Southeast Energy Authority, along with other substantial offerings from various districts. The San Diego Community College District alone has issued $850 million in general obligation bonds. Interestingly, the competitive bond sales are also making headlines, specifically noting the Tri-County Regional Vocational Technical School District, Massachusetts, leading with $144 million in school project loans.

In December, as municipal yields swelled by an average of 37 basis points, particularly in the 15-20 year range, it became evident that municipal bonds remain an attractive albeit historically expensive avenue for investors. Jason Wong of AmeriVet Securities emphasized that while yields have increased, the comparison to U.S. Treasuries indicates that the municipal marketplace retains significant value propositions despite rising costs. This dynamic complicates investor decision-making, as the allure of higher yields is counterbalanced by the ongoing financial metrics.

Redemption trends are shaping the near-term outlook for municipal bonds. This January is predicted to experience a “modest surge” in redemption activity, highlighting that bond holders will receive an estimated $16.3 billion in redemptions against $11.8 billion in interest payouts. Pat Luby of CreditSights remarked on the implications of these retractions from the bond markets, especially given that major states like Illinois, Texas, and New Jersey will represent significant portions of the redemptions this month.

As redemptions typically generate heightened liquidity in the market, investors may have opportunities to reinvest in newly issued bonds. However, continued outflows from municipal mutual funds indicate investor trepidation in the face of fluctuating interest rates and significant economic uncertainties. The historically mixed performance of municipal bonds in January, alternating between substantial profits and losses, adds another layer of complexity for investors contemplating the coming weeks.

The overarching influence of governmental monetary policy is expected to loom large in 2025, creating a climate of caution among investors. There are substantial concerns surrounding potential changes in the tax exemption status of municipal bonds due to impending political shifts, which could simultaneously impact supply and, ultimately, the performance of the asset class. The Federal Reserve’s cautious stance towards inflation and labor market stability could prompt a pause in bond interest rate adjustments, further stabilizing the market amidst the financial ambivalence.

Historical trends suggest that returns on municipal bonds tend to hover around a modest average of 0.4% per annum over the past decade. With the potential for volatility stemming from external economic force, coupled with internal market dynamics, investors must carefully evaluate their strategies and exposure in municipal bonds. Noteworthy is the observation that 2025 may offer a unique landscape for the municipal sector, particularly if the administration introduces changes that impact tax legislation.

As the market prepares to embrace new issuance and contend with recent shifts in the financial landscape, the outlook for municipal bonds remains captivatingly complex. Investors must navigate these nuances with diligence and foresight as they chart their course through the early weeks of 2025.