The municipal bond market experienced minimal changes on Thursday as the largest deals were finalized. Despite this, municipal bond mutual funds reported a return to outflows. U.S. Treasury yields declined while equities saw an increase near the market close. The ratios of municipal bond yields to Treasury yields varied on Thursday, with the two-year at 66%, the three-year at 66%, the five-year at 67%, the 10-year at 66%, and the 30-year at 84%. These numbers provide insight into the market dynamics and investor sentiment at the time.

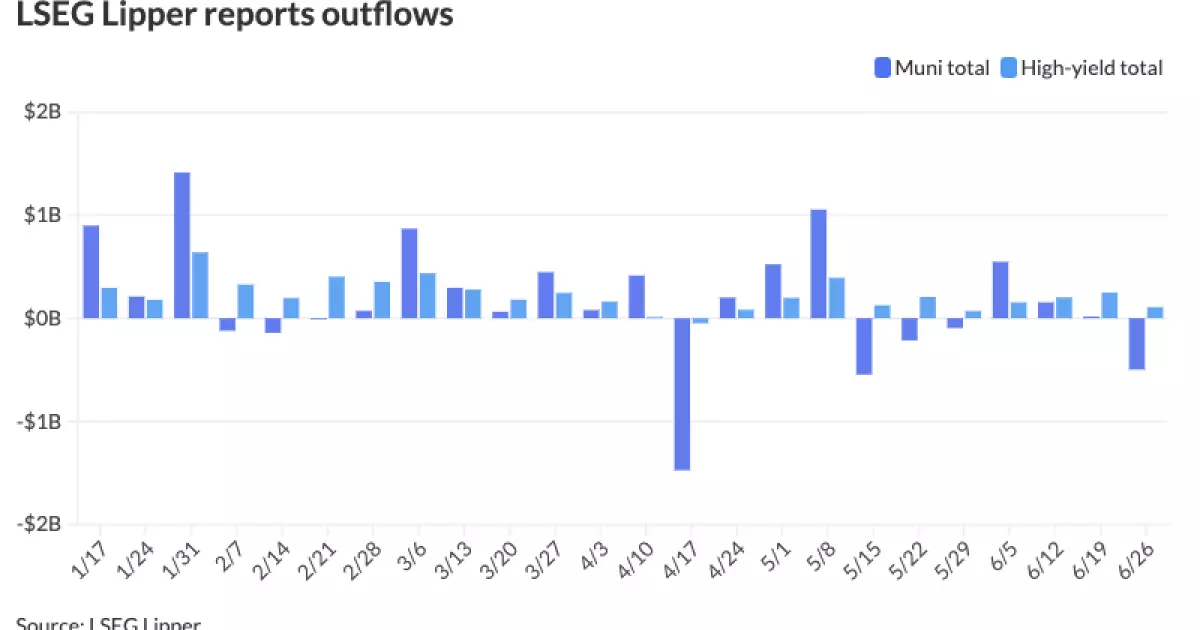

Municipal bond mutual funds faced outflows as investors withdrew $498 million from the funds after experiencing $16 million in inflows the previous week. The outflows were primarily driven by long-term funds. However, high-yield bonds continued to demonstrate strength, attracting inflows of $107 million following $248.9 million in inflows the week before. The slowdown in investment demand is not unexpected, as noted by Pat Luby, the head of municipal strategy at CreditSights. The recent Federal Open Market Committee meeting and the holiday-shortened week have distorted market conditions, making it challenging to accurately gauge demand dynamics.

The market saw a surging new-issue calendar of over $12 billion to close out June, contributing to six months of issuance gains. Noteworthy deals included the John F. Kennedy International Airport New Terminal One Project, which had unique features that boosted demand. Additionally, there was significant appetite for AMT paper. The primary market also witnessed several major transactions, such as senior sales tax bonds from the Massachusetts Bay Transportation Authority, revenue refunding bonds from the State Building Authority of Michigan, and unlimited tax school building bonds from the Lewisville Independent School District, among others. These deals provided insights into the diverse offerings in the market.

Preliminary data for June indicated an increase in issuance compared to the previous year. The market is expected to experience lighter holiday supply weeks followed by heavier volume weeks, impacting the flow of reinvestment capital. The influx of reinvestment capital during the first half of July is anticipated to be significant, with payments expected to surpass those in August. The upcoming months will see a balance of reinvestment capital from refunding activities. Analysts project a mix of varying payment levels throughout the summer, highlighting the importance of monitoring these trends for market participants.

Various sources reported different figures for municipal bond yields and Treasury yields, providing a comprehensive view of the market’s performance. Despite minor fluctuations, the overall trend indicated stability and relative consistency within the market. Treasury yields were firmer at the time, with varying rates across different maturity periods. These metrics serve as essential indicators for investors and market analysts to assess the current state of the municipal bond market.

Overall, the municipal bond market exhibited a mix of stability and volatility, influenced by various economic factors and investor behaviors. The influx of new issuances, changing demand dynamics, and Treasury yield movements all contributed to the market’s fluidity. Monitoring these trends and developments is crucial for market participants looking to make informed decisions in the dynamic municipal bond market environment.