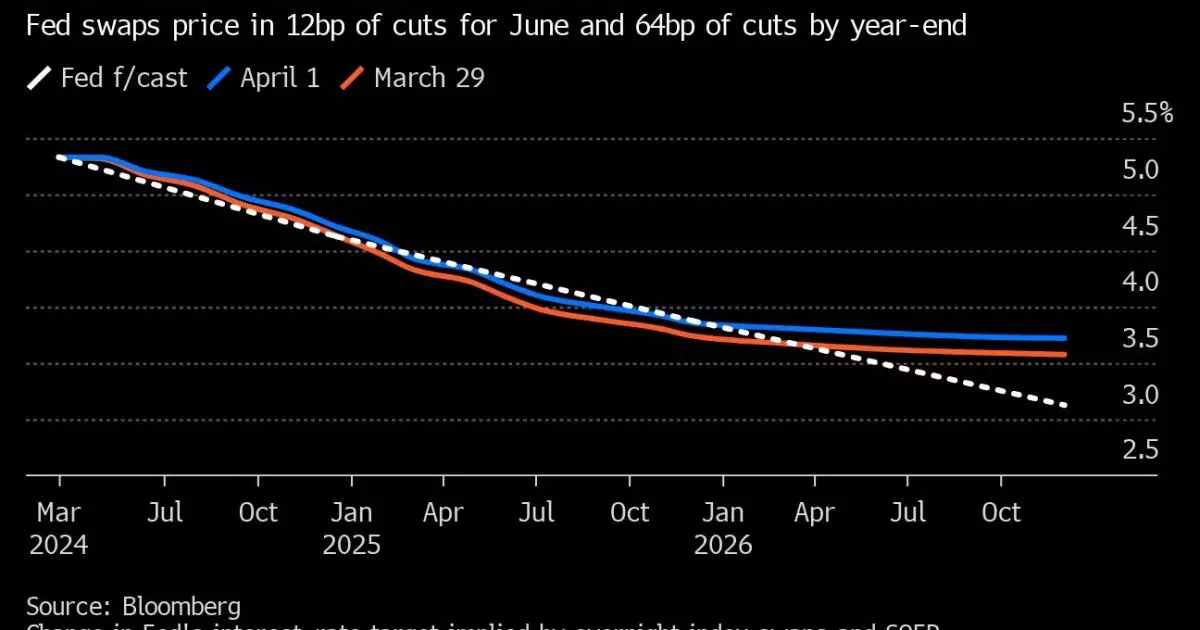

Following the recent gauge of U.S. manufacturing activity showing expansion for the first time since 2022, bond traders have adjusted their expectations for monetary policy easing by the Federal Reserve. The amount of Fed easing priced into swap contracts for this year dropped to fewer than 65 basis points, which is less than what Fed policy makers themselves have forecasted. Additionally, the odds of a first rate cut in June briefly fell below 50%, reflecting a significant shift in market sentiment.

The release of the ISM manufacturing data caused a bond-market selloff, leading to a notable increase in two- to 30-year Treasury yields. This selloff was already in motion before the data release as traders reassessed the outlook for monetary policy based on economic indicators and recent comments by Fed Chair Jerome Powell. The market reacted strongly to the unexpected strength in manufacturing activity, signaling a potential change in the Fed’s stance on interest rates.

The ISM report contributes to the narrative of the economy’s resilience, which has implications for the Fed’s monetary policy decisions. The data suggests that the Fed may adopt a more patient approach given the strength of the economy. Recent developments, such as strong personal income and spending data for February, reinforce the idea that the Fed is hesitant to cut rates prematurely. The upcoming release of March employment data is anticipated to show a slowdown in job creation, but the unemployment rate remains at historically low levels.

In addition to the impact on government bonds, the recent uptick in corporate bond offerings is putting pressure on Treasuries. The surge in private borrowing indicates that interest rates are not a significant constraint for U.S. companies, adding to the upward pressure on yields. This trend, coupled with the Treasury market’s first monthly gain since December, reflects the complex interplay between economic data, market expectations, and monetary policy decisions.

Shift in Market Sentiment

The market has undergone a significant shift in sentiment since the beginning of the year when expectations for Fed rate cuts were much higher. The initial projection of 150 basis points in easing for 2024 has now been recalibrated based on more positive growth data and a less pronounced decline in inflation. The market stabilization in March, after a period of uncertainty in January and February, underscores the evolving nature of market dynamics and the importance of staying attuned to changing economic indicators.

The recent strength in U.S. manufacturing activity has had a notable impact on bond traders’ expectations for Fed policy. The market reaction, coupled with other economic developments, underscores the complexity of forecasting monetary policy decisions and highlights the importance of closely monitoring economic data and central bank communications. Bond traders will need to remain vigilant in assessing evolving market conditions and adjusting their strategies accordingly to navigate the changing landscape of monetary policy and economic indicators.