As we step into 2025, the municipal bond market is imbued with a diverse set of dynamics that merit close examination. Investors have begun to adjust their strategies as they grapple with changing economic conditions, shifting interest rates, and fluctuating demand. Last year, we witnessed a descent into market losses, particularly towards December’s end, yet municipal bonds ended 2024 with a positive net performance. Understanding these trends is crucial for both seasoned investors and newcomers alike, as the municipal sector offers unique opportunities and challenges.

The year commenced with a stronger sentiment among municipal bond investors, buoyed by the influx of reinvestment dollars typically seen in January. This renewed optimism stands against a backdrop of U.S. Treasury fluctuations that shaped investor decisions. While many anticipated an economically vibrant year, the bond market’s mixed performances reveal the complexities of investor sentiments. High-yield municipal funds demonstrated resilience despite facing outflows earlier, rebounding with notable inflows right before the year’s end.

A critical element defining the current landscape is the movement of municipal yields compared to U.S. Treasuries. Reports indicated that yields for triple-A rated bonds decreased by one to three basis points across various maturities on January 5, 2025, signaling a potential long-term shift in investor preferences. Particularly significant is the observation by people like Kim Olsan from NewSquare Capital, who underscored that high-grade bonds in the ten-year range opened above the 3% mark — a high not seen since 2010. This shift poses questions about what long-term indicators, such as inflation and interest rate policies, might influence yield adjustments throughout the upcoming year.

The completion of 2024 wrapped up with a mixed performance for municipal bonds. Despite a total return of -1.46% for December, the overall annual return came in at +1.05%. Notably, this performance exceeded U.S. Treasuries yet fell short of corporate bonds, suggesting that municipal bonds maintained a stable appeal despite various challenges. Peter DeGroot from J.P. Morgan presents insights into how specific asset classes within municipals, such as riskier IDR and BBB sectors, outperformed expectations in contrast to the broader market.

Another layer of complexity arises from the impact of duration on overall returns. As noted by Olsan, long-duration bonds suffered significant losses in December, losing 2.4% compared to their intermediate counterparts. The steep decline in long-dated indices highlights the crucial shift investors must navigate. The flattened slope of the 30s10s MMD curve indicates an evolving risk perception among investors, especially in the context of potential interest rate hikes that could further dissuade long-term investments.

Despite a challenging year-end, Bloomberg’s High Yield Municipal Index closed 2024 with a respectable 6.32% total return, showcasing the benefits of diversifying into riskier asset tiers. Although December brought negative returns of -1.66%, the prior performance of high-yield munis indicates stabilization within this segment. As Olsan suggests, high-yield munis exemplified resilience with positive inflows for most of 2024, making them compelling options for investors looking to balance safety with yield.

The Impact of Economic Conditions on Market Outlook

Looking ahead, the sustainability of the municipal bond market’s performance is inextricably linked to economic stability. Olsan reiterates that a favorable economic landscape is vital for preserving the revenue streams associated with municipal projects, suggesting that the trajectory of interest rates is a primary determinant for 2025 performance. With the potential for renewed supply from the municipal sector should UST rates fall, the interplay between bond yields and economic indicators becomes increasingly vital.

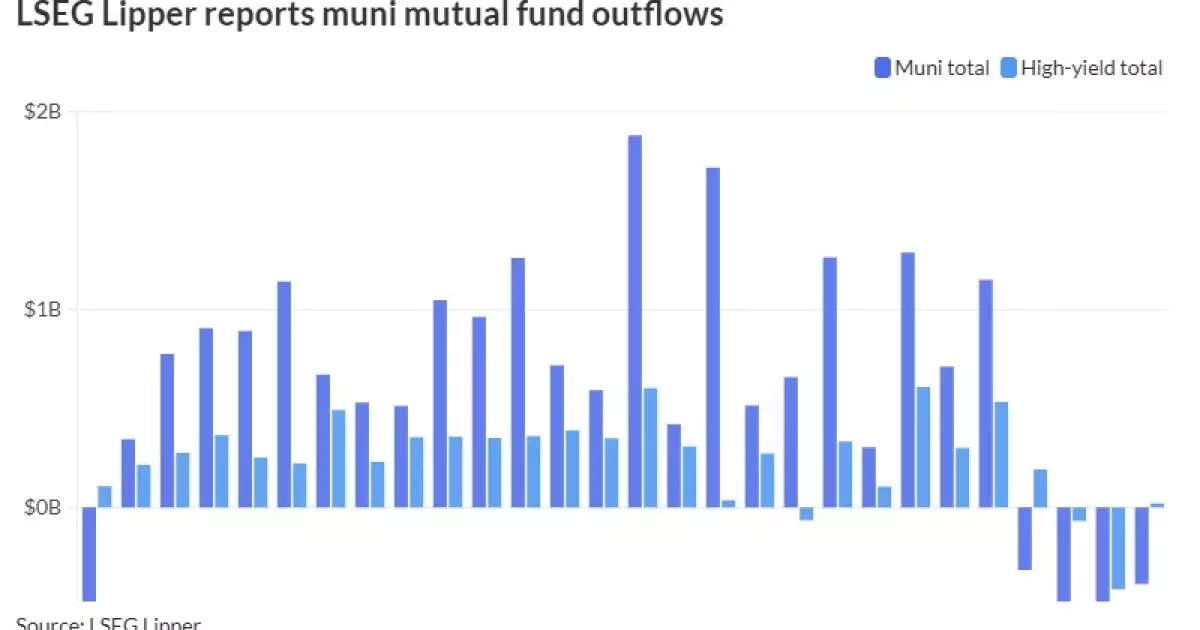

The trends in fund flows during December reveal a notable turn of events, with substantial outflows reported after a lengthy period of inflows. Measuring investor sentiment, LSEG Lipper reported a loss of $386.9 million in municipal bond mutual funds, correlating with rising interest rates that deterred investments. This shift shows how swiftly market sentiments can change, especially under economic pressures. Fund flow analyses expose the delicate balance between investor confidence and market performance.

As 2025 unfolds, the landscape of municipal bonds presents an intricate blend of challenges and opportunities. With yields beginning to stabilize, and the market still recovering from the shock of previous downturns, investors need to remain vigilant. Understanding local market dynamics, duration risk, and economic indicators will be vital in navigating this space. The ability to adapt strategies in response to evolving conditions may very well determine investment success in the year ahead.