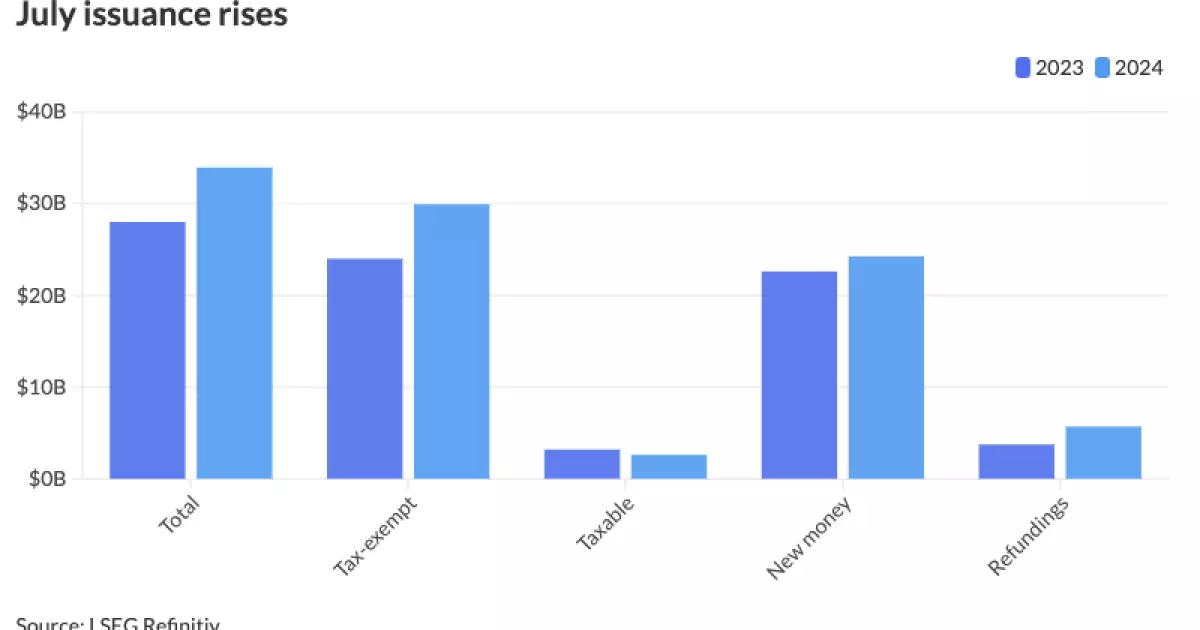

The month of July saw a significant increase in municipal bond issuance volume, marking the seventh consecutive month of climbing issuance. Several factors contributed to this rise, including front-loaded issuance ahead of the election, a lower rate environment, and a breakneck pace of supply. July’s volume reached $33.935 billion in 576 issues, up 21.2% from the previous year. This surge in issuance reflects the heightened activity in the municipal market driven by market conditions and issuer behavior.

According to Sudip Mukherjee, a senior fixed-income strategist at UBS, the current pace of issuance is the highest since the financial crisis. He attributes this trend to the summer technicals and redemption demand, which have offset the large supply entering the market. Mukherjee also highlights how issuers have been motivated to come to market to take advantage of the declining rates, stimulating their desire to push deals forward. Additionally, the uncertainty surrounding the upcoming election has led issuers to front-load issuance to avoid potential rate volatility.

Jeff Timlin, a managing partner at Sage Advisory, pointed out that the market has already factored in a Federal Reserve rate cut in September. However, there is a risk for issuers if the projections change and rate cuts are postponed, resulting in higher rates. Timlin emphasized the importance of staying vigilant in a dynamic market environment to make informed decisions about issuing bonds.

Chad Farrington, co-head of municipal bond investment strategy at DWS, commented on the unexpected surge in issuance week after week, indicating that it has surpassed last year’s levels. He speculated on the possibility of volume returning to a more stable level of $10 billion in the following weeks. Traditionally, summer months experience a drop in supply, followed by an increase in issuance as the fall approaches. However, this year has seen strong and steady issuance in June and July, challenging the seasonal patterns in the market.

Looking ahead, Sudip Mukherjee predicts that the pace of issuance will moderate but remain elevated compared to the previous year. The demand for municipal bonds continues to be robust, driven by various factors such as market conditions, economic outlook, and issuer preferences. As market participants navigate the evolving landscape, they must adapt to changing conditions and make strategic decisions to optimize their bond offerings.

In July, tax-exempt issuance amounted to $29.933 billion in 521 issues, representing a 24.8% increase from the previous year. On the other hand, taxable issuance decreased by 18.2% to $2.607 billion in 50 issues. Alternative-minimum tax issuance rose significantly by 67.4% to $1.395 billion, underscoring the diverse nature of bonds being issued in the market.

New-money and refunding volumes showed mixed trends, with the former increasing by 7.3% and the latter rising by 52.2%. Revenue bond issuance surged by 46.3% to $23.166 billion, while general obligation bond sales declined by 11.5%. Negotiated deal volume and competitive sales both experienced substantial growth, indicating healthy market activity across different issuance channels.

In terms of geographic distribution, California led the states in issuance volume year-to-date, followed by Texas, New York, Florida, and Massachusetts. These states have seen significant increases in issuance compared to the previous year, reflecting the diverse landscape of municipal bond issuance across the country. Overall, the municipal market continues to be vibrant and dynamic, with issuers adapting to changing market conditions to meet investor demand and optimize their financing strategies.