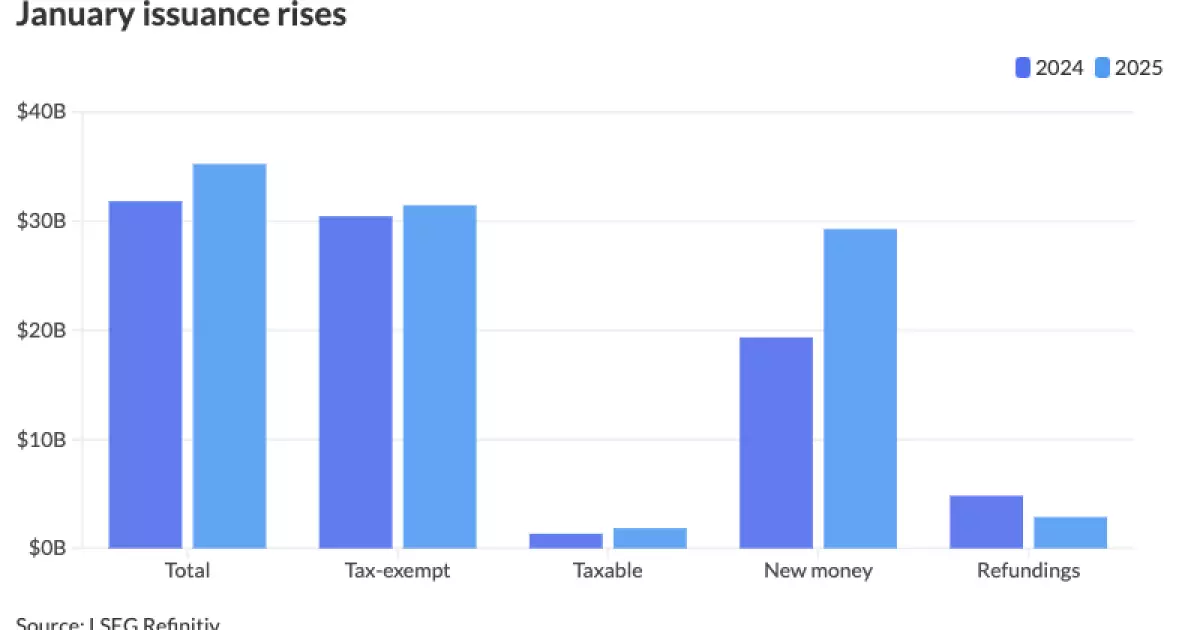

The municipal bond market began 2025 with a notable surge, as evidenced by the issuance figures released for January. The growth in issuance, which amounted to $35.243 billion across 486 individual issues, reflects a year-over-year increase of 10.8% from the previous year’s $31.817 billion in 554 issues. This boost not only exceeds the historical 10-year average of $28.675 billion for January but also signifies a considerable confidence among issuers as they navigate a landscape filled with fiscal uncertainties and potential tax changes.

Analysts point out that issuers are eager to take action before potential volatility escalates. As Alice Cheng, a credit analyst at Janney, noted, the anticipation surrounding Federal Open Market Committee (FOMC) meetings and the overall impact of policy changes has prompted many to act rather than wait. The uncertainty revolving around interest rate adjustments compounded by policy implications from the current administration has made the market ripe for more aggressive issuance behaviors.

Navigating Economic Uncertainties

Interest rate levels, currently held between 4.25% and 4.50%, remain a crucial factor influencing the municipal bond market. Holder of the highest office, President Donald Trump, has indicated a desire for rate cuts, adding to the pressure that issuers feel while making significant financial decisions. The fear of funds from the Infrastructure Investment and Jobs Act potentially being retracted only adds another layer of urgency for issuers to proceed with offerings, as they seek to lock in opportunities amidst the current climate of uncertainty.

Moreover, the taxation landscape plays a critical role as well in determining issuers’ behaviors. With rumors of targeted tax changes potentially impacting sectors such as healthcare and higher education, concerns surrounding the status of tax exemptions have led many to accelerate their issuance plans. James Pruskowski, chief investment officer at 16Rock Asset Management, indicated that the current brisk pace of issuance correlates with a need to mitigate risks associated with forthcoming policy shifts.

A significant driver of the January issuance increase stems from a pent-up demand within the market. After a year in which issuance was hampered by volatility, issuers are eager to capitalize on ‘missed opportunities,’ especially following a robust December where many deals were likely postponed until the new year. Industry observers note that as market volatility begins to subside, more issuers feel empowered to raise capital.

COVID-era benefits have started to dwindle, compelling municipalities to tap into the capital markets for needs previously funded by these programs. The January issuance surge not only indicates a robust start for 2025 but also suggests that forthcoming months may reveal a sustained growth trajectory, as echoed by Barclays strategist Mikhail Foux, who predicts healthy visibility in the pipeline.

The impact of federal funding continues to resonate within municipal frameworks. Rob Dailey, head of PNC Public Finance, pointed out that governments benefiting from federal infrastructure dollars are seizing the momentum to initiate related projects, which can drive appetite in both the bond market and broader credit environments. These auxiliary projects—including transit improvements, affordable housing developments, and other state-level initiatives—are positioned to sustain demand in the bond market for the foreseeable future.

Data reveals that tax-exempt issuance in January reached $31.45 billion across 428 issues, demonstrating a 3.3% increase from the previous year. Taxable issuance also rose significantly, marking a 36.7% increase to $1.849 billion across 54 issues. Notably, new-money issuance soared by 51.4%—a clear indicator of the eagerness to fund capital projects and infrastructure needs as we embark on this new year.

Significant growth was not uniform across all states, but certain regions, such as California, emerged as leaders in the issuance landscape. With $6.371 billion in issuances—an increase of 12.6% year-over-year—California stands at the forefront. Texas follows as the second-largest issuer, while Florida’s remarkable 115.1% spike in issuance highlights the varying regional dynamics that drive state-specific issuance rates.

Conversely, Massachusetts has seen a notable decrease, falling 50.2% from the previous year, attesting to the diverse challenges individual states face. Meanwhile, states like Ohio and Colorado have reported impressive percentage increases, showcasing the uneven recovery and opportunities that persist across the municipal bond ecosystem.

As we reflect on January’s issuance figures and the factors driving them, the municipal bond market faces a promising outlook for 2025, with expectations of sustained activity as issuers navigate economic uncertainties and capitalize on available opportunities. Factors such as federal dollars and pent-up demand position the market favorably, indicating that we may see continued engagement in the municipal bond sector as the year progresses. It is clear that the trends set in motion during January will likely resonate throughout the year, shaping the future landscape of municipal finance.