The municipal bond market has experienced significant shifts throughout 2024, culminating in a notable decline in issuance during November. As we approach the end of the year, it’s essential to dissect the factors that have influenced these trends, particularly as we navigate the complexities surrounding election-related volatility and market conditions.

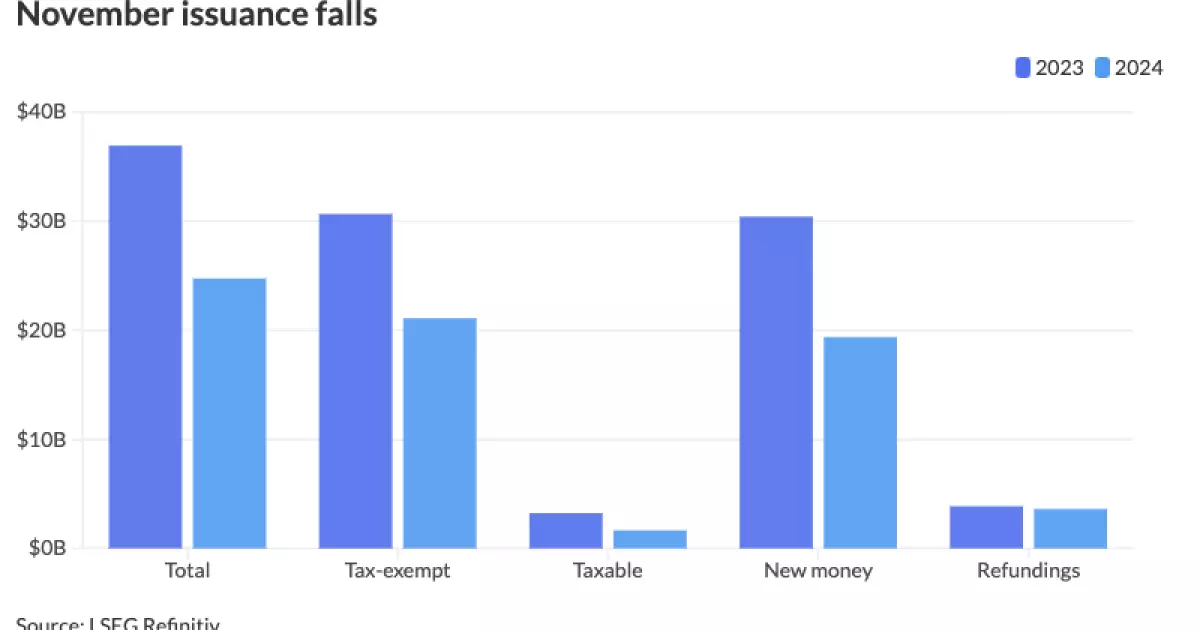

November 2024 recorded a substantial fall in bond issuance, totaling $24.743 billion across 607 issues, which represents a dramatic 33% drop compared to November 2023’s $36.918 billion from 822 issues. This decline marked the first year-over-year decrease in issuance for 2024 and positioned November as the lowest monthly total for the year. By contrast, the year-to-date figures suggest a robust upward trajectory, with $474.755 billion issued thus far, reflecting a 32.8% increase over the previous year. Despite the November decline, projections indicate that total issuance for 2024 is on track to potentially exceed the historic figure of $484.601 billion set in 2020, with estimates suggesting it could approach or even surpass $500 billion.

Several key contributors have been identified as pivotal in the November downturn. A significant factor was the constraint of available pricing days during the month. According to Tom Kozlik, head of public policy and municipal strategy at HilltopSecurities, the market faced challenges due to the election cycle and the Federal Open Market Committee’s meeting, which curtailed the time available for issuers to launch new deals effectively. The latter part of the month was also impacted by the Thanksgiving holiday, leading to reduced activity across the board.

Chad Farrington, co-head of municipal bond investment strategy at DWS, noted that while there were heavier supply weeks immediately preceding and following the aforementioned events, the cumulative effect of these disruptions has resulted in insufficient issuance opportunities. This suggests that the decrease in November does not necessarily reflect a lack of issuer enthusiasm; rather, it highlights the timing and operational impacts of external events.

Election-related volatility has played a crucial role in shaping the municipal bond market, particularly in November. In the lead-up to elections, there was a marked spike in issuance as issuers aimed to capitalize on favorable market conditions before potential policy changes could take effect. Interestingly, though initial predictions anticipated a more turbulent market environment post-election, the reality has been a relatively stable turn, albeit accompanied by heightened policy uncertainty moving forward.

Kozlik articulated that what began as concern over election results has now transitioned into apprehension regarding future tax policies, particularly the jeopardized status of the municipal tax-exemption. This shift may fuel additional issuance activity as issuers rush to lock in tax-exempt financing before any legislative changes are implemented in 2026.

Predictions and Future Outlook

Looking ahead to December, the anticipated issuance volume could range between $20 billion and $30 billion, according to Kozlik’s projections. However, the looming threat of shifting tax-exempt statuses could provoke issuers to act quickly, reminiscent of the spike seen in December 2017, when new tax legislation prompted a last-minute surge in municipal activity.

Industry analysts have begun formulating forecasts for 2025, with broad consensus anticipating a return to issuance figures around $500 billion. However, there remains divergence in predictions; some forecasters, like Kozlik, predict issuance could soar to $745 billion if significant tax policy changes are introduced, triggering an influx of issuers seeking to finalize tax-exempt deals before potential limitations come into force.

Conversely, Matt Fabian of Municipal Market Analytics anticipates a more conservative issuance range between $250 billion and $300 billion if tax-exempt barriers are enacted sooner than planned. This disparity underscores the uncertainty embedded within the municipal bond landscape, making accurate forecasting increasingly challenging.

California has emerged as the leader in year-to-date issuance with $68.902 billion, followed closely by Texas and New York. The trends at the state level reflect broader economic conditions and investor confidence. As municipalities grapple with the implications of upcoming elections and potential tax reforms, their strategies will inevitably impact the overall health of the bond market.

While November 2024 saw a decline in municipal bond issuance driven by election-induced uncertainties and constrained pricing opportunities, the overarching landscape remains poised for record-breaking numbers by year-end. The interplay between issuer decisions and external market forces will define the narrative as we transition into 2025, with the ongoing uncertainty around tax-exempt status likely catalyzing a flurry of end-of-year activity. The evolution of municipal issuance will remain closely monitored as stakeholders aim to navigate this complex environment.