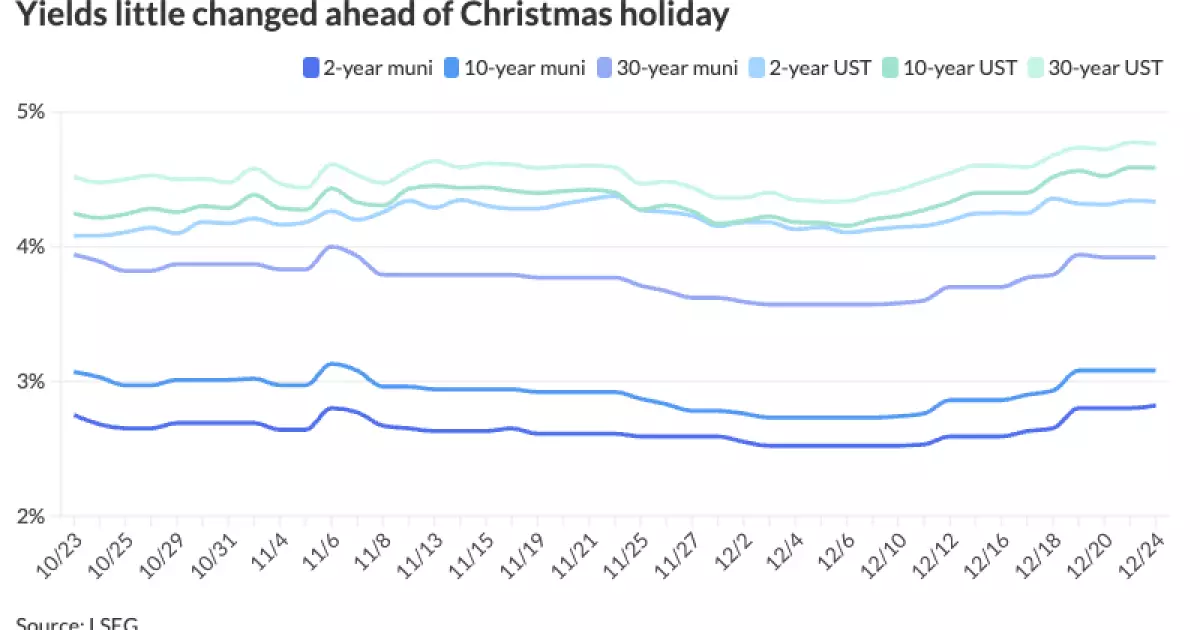

As we approach the final weeks of 2024, the municipal bond market has exhibited a mix of stability and slight decline. Recent trends show that while U.S. Treasuries have performed slightly better, the yields on top-tier municipal bonds have crept upwards by a basis point or two. The municipal-to-Treasury yield ratios also indicate a stable yet cautious market, hovering around 65% for shorter maturities and peaking at 82% for 30-year bonds. This nuanced landscape reveals the delicate balance between municipal bonds and Treasuries as investors weigh their options in a fluctuating economic environment.

According to Kim Olsan, a senior fixed income portfolio manager at NewSquare Capital, the pressures on taxable rates do not necessarily translate to an adverse effect on municipal bonds; rather, demand for municipal bonds appears stable. The 10-year UST yielding 4.60%, down from an earlier peak, highlights the changing dynamics of asset allocation where tax-exempt yields are now firmly positioned above 3.00%. Such figures indicate that investors are responding strategically to the current yield environment, moving towards longer maturities as tax-exempt yields reach their highest levels in a considerable timeframe.

In recent trading sessions, there has been a notable increase in activity, with a staggering 67% of secondary trades involving maturities beyond 2030. This shift suggests a strategic pivot by investors who may be looking to capitalize on the steeper slopes of the yield curve, particularly within the 10 to 20-year range. The current market dynamics echo historical trends whereby investors favor longer-dated securities, a strategy reinforced by the higher yield differentials now being offered under these conditions.

Moreover, marketplace statistics indicate a growing appetite for fund deployment as recent figures show floating rates rising to nearly 3.75%. When compared to levels just weeks prior, this represents an encouraging shift, as it underscores a proactive response to increasing yields within the longer maturity segment. The stability of demand for these longer-dated bonds is pivotal, as it signifies confidence amid fluctuating economic currents.

As we gaze into the crystal ball for 2025, the interplay of Treasury rates, broader economic conditions, and market technicalities will define municipal bond opportunities. The strategic insights offered by UBS strategists underscore an increased level of uncertainty typically associated with election years, particularly around fiscal and tax policies. This apprehension may influence the muni market, although potential alterations to tax-exempt statuses are predicted to have limited widespread effects.

With federal deficit concerns looming large, there lies a potential risk where inflation could rear its head due to increased tariffs and fiscal discrepancies. UBS highlights that what happens in 2025 will heavily depend on the actions of fiscal moderates within the Republican party and how they approach aggressive protectionist measures. These macroeconomic elements will likely shape market sentiment and investment decisions throughout the upcoming year.

On the supply side, an expectation of over $450 billion in tax-exempt issuance surfaces as infrastructure continues to demand funding. However, municipalities must navigate the delicate task of prioritizing spending, particularly as certain fiscal aids from programs like the American Rescue Plan come with stipulations that demand careful allocation of resources. The decisions made in this regard could have far-reaching implications for municipal credit quality.

While the market has recently seen some sell-offs, expectations from firms like UBS suggest that AAA municipal bond yields might decline moderately in 2025. The current ratios still appear relatively high compared to historical benchmarks, suggesting a degree of richness that temporary market shifts might affect, yet likely not drastically. Analysts suggest credit spreads will remain stable owing to expected economic resilience, putting emphasis on the underlying strength of several municipal issuers that continue to possess healthy liquidity positions.

Nevertheless, a cautionary note emerges regarding municipalities that may have allocated previously received funds to ongoing operational expenses rather than one-off investments. This choice could lead to challenges once these funds are depleted, potentially triggering a need for additional revenue sources or necessitating cuts in public services.

Ultimately, for savvy investors and issuers alike, a thorough understanding of the municipal bond market’s current landscape and foresight into potential economic shifts will be crucial as we move into 2025. As the interplay between yield movements, market demand for longer maturities, and upcoming fiscal challenges continues to evolve, new opportunities will emerge. By maintaining a strategic perspective and remaining alert to ongoing market developments, investors can navigate the complexities of the municipal bond space with informed confidence, capitalizing on the nuanced changes that characterize this vital segment of the financial landscape.